Preliminary Offering Circular, Dated March 16, 2018

An offering statement pursuant to Regulation A relating to these securities has been filed with the Securities and Exchange Commission. Information contained in this Preliminary Offering Circular is subject to completion or amendment. These securities may not be sold nor may offers to buy be accepted before the offering statement filed with the Commission is qualified. This Preliminary Offering Circular shall not constitute an offer to sell or the solicitation of an offer to buy nor may there be any sales of these securities in any state in which such offer, solicitation or sale would be unlawful before registration or qualification under the laws of any such state. We may elect to satisfy our obligation to deliver a Final Offering Circular by sending you a notice within two business days after the completion of our sale to you that contains the URL where the Final Offering Circular or the offering statement in which such Final Offering Circular was filed may be obtained.

![]()

GENERATION INCOME PROPERTIES, INC.

$20,000,000

4,000,000 SHARES OF COMMON STOCK

$5.00 PER SHARE

Explanatory Note

This Offering Circular is part of the post-qualification amendment we filed in order to update the financial statements contained herein in accordance with Rule 252(f)(2)(i) of Regulation A. In addition to updating the financial statements presented herein, this amendment updates portfolio, financial and statistical data, updates the plan of distribution, and extends the offering termination date to May 1, 2018. All material terms of this offering otherwise remain the same.

Generation Income Properties, Inc., a Maryland corporation, is an internally managed net lease company organized in June 2015 to opportunistically acquire and invest in freestanding, single-tenant commercial properties net leased to investment grade tenants.

This offering circular constitutes the initial public offering (“IPO”) of GENERATION INCOME PROPERTIES, INC. (the “Company”, “us”, “we”) common stock. This offering is being conducted pursuant to an exemption from registration under Regulation A of the Securities Act of 1933, as amended.

We are offering 4,000,000 shares of our common stock at an offering price of $5.00 per share for a total amount of $20,000,000. We do not intend to use an underwriter or broker dealer in connection with this offering. We will offer on a “best efforts” basis, up to 4,000,000 shares of our common stock, par value $0.01 per share, to purchasers in this offering, to be issued in one or more closings. As of the date of this offering circular we have issued 791,267 shares of common stock in exchange for gross proceeds totaling $3,956,335. Prior to this offering, there has been no public market for our common shares. Our sole executive officer will use his best efforts to sell the securities offered. There is no requirement to sell any specific number or dollar amount of securities and we may sell less than $20 million of our common stock. We will pay all expenses incurred in this offering.

The sale of shares pursuant to this offering began on approximately March 3, 2016, and, upon qualification of the post-qualification amendment to our offering statement of which this offering circular is a part, will continue until the earlier of (i) the date on which all of the shares offered hereby have been sold, or (ii) May 1, 2018. We may, however, terminate the offering at any time and for any reason. At this time, there is no public trading market for shares of our common stock. There is no minimum required sale.

We intend to elect and qualify to be taxed as a real estate investment trust (“REIT”), for federal income tax purposes. To assist us in qualifying as a REIT, among other reasons, ownership of our outstanding common shares by any person is limited to 9.8%, subject to certain exceptions. In addition, our articles of incorporation contain various other restrictions on the ownership and transfer of our common shares.

Our director and president, David Sobelman, will be responsible for marketing and selling these securities. The securities are offered on a best efforts basis, which means that Mr. Sobelman will use his best efforts to sell the common shares to the public. The shares will be offered at a fixed price of $5.00 per share for the duration of the offering, and there will be no minimum number of shares required to be sold to close the offering. Any funds received from the sale of shares will be immediately available for use by us.

SHARES OFFERED |

| PRICE TO |

| SELLING AGENT |

| PROCEEDS TO |

| ||

BY COMPANY |

| PUBLIC |

| COMMISSIONS (1) |

| THE COMPANY(2) |

| ||

Per Share |

| $ | 5.00 |

| $0.00 |

| $ | 5.00 |

|

Minimum Purchase |

| None |

| $0.00 |

| Not applicable |

| ||

Total (4,000,000 shares) |

| $ | 20,000,000 |

| $0.00 |

| $ | 20,000,000 |

|

(1) | We do not intend to use commissioned sales agents or underwriters. |

(2) | Does not include expenses of the offering including approximately $100,000 from the proceeds of the offering to reimburse Mr. Sobelman for legal, accounting, and sales and marketing expenses he incurred on our behalf in connection with the formation of our company and this offering. |

The proceeds from the sale of the securities will be placed directly into our account. All proceeds from the sale of the securities are non-refundable, except as may be required by applicable law. We intend to apply for quotation of our common stock on the over-the-counter market (“OTC”) through the OTC Bulletin Board (“OTCBB”), or OTC Markets Group OTCQX or OTCQB. We will require the assistance of a market-maker to apply for quotation and there is no guarantee a market-maker will assist us.

Investing in our common shares involves risks. You should read the section entitled “Risk Factors” beginning on page 11 of this prospectus to read about factors you should consider before investing in our common shares, including:

• | Our president will face conflicts of interest, since he is our sole officer and directors and owns the majority interest in and serves as the managing member of 3 Properties, LLC, a real estate investment brokerage firm. |

• | We currently have no employees and will initially rely on our sole officer and director and other paid outside consultants to manage our business and assets. |

• | We have no prior operating history and there is no assurance that we will be able to achieve our investment objectives. We may change our operational policies (including our investment guidelines, strategies and policies) without stockholder consent at any time. |

• | Because this is a “blind pool” offering, you will not have the opportunity to evaluate our investments before we make them. We currently own one property and have one property under contract. |

• | We may pay distributions from sources other than cash flow from operations, including, without limitation, the sale of assets, borrowings or offering proceeds. |

• | You may not own more than 9.8% in value of the outstanding shares of our common stock or more than 9.8% of the number or value of any class or series of our outstanding shares of stock. Therefore, your ability to control the direction of our company will be limited. |

• | We cannot guarantee that a liquidity event will occur. Our shares will not be listed at the time of purchase and you will have no immediate liquidity until such time as our shares are listed, if at all, on a registered national securities exchange upon qualification or for quotation on the Over-The-Counter Bulletin Board. |

• | Qualifying as a REIT involves highly technical and complex provisions of the Internal Revenue Code, and our failure to qualify as a REIT or remain qualified as a REIT would subject us to U.S. federal income tax and applicable state and local taxes, which would reduce the cash available for distribution to our stockholders. |

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act, which became law in April 2012, and will be subject to reduced public company reporting requirements. See “Jumpstart Our Business Startups Act” contained herein.

Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

You should rely only on the information contained in this offering circular. We have not authorized anyone to provide you with information different from that contained in this prospectus.

[2]

TABLE OF CONTENTS

PROSPECTUS SUMMARY | 4 |

|

|

THE OFFERING | 9 |

|

|

RISK FACTORS | 11 |

|

|

OUR BUSINESS | 31 |

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 40 |

|

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 53 |

|

|

DESCRIPTION OF SHARES | 56 |

|

|

OUR OPERATING PARTNERSHIP AND THE PARTNERSHIP AGREEMENT | 61 |

|

|

MATERIAL FEDERAL INCOME TAX CONSIDERATIONS | 63 |

|

|

ERISA CONSIDERATIONS | 81 |

|

|

EXPERTS | 86 |

|

|

WHERE YOU CAN FIND MORE INFORMATION | 86 |

|

|

REPORTS TO SHAREHOLDERS | 86 |

|

|

INDEX TO FINANCIAL STATEMENTS | F-1 |

[3]

ABOUT THIS OFFERING CIRCULAR

You should rely only on the information contained in this offering circular. We have not authorized anyone to provide you with different or additional information. If anyone provides you with different or inconsistent information, you should not rely on it. Neither we, nor anyone working on our behalf, are making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this offering circular prepared by us is accurate only as of their respective dates or on the date or dates which are specified in these documents. Our business, financial condition, liquidity, results of operations and prospects may have changed since those dates.

MARKET DATA

We use market data and industry forecasts and projections throughout this offering circular, and in particular in the sections entitled “Prospectus Summary,” “Market Opportunity” and “Business and Properties.” We have obtained substantially all of this information from independent industry sources and publications as well as from research sources prepared by third party industry sources. Any forecasts are based on data (including third party data), models and experience of various professionals, and are based on various assumptions, all of which are subject to change without notice. In addition, we have obtained certain market and industry data from publicly available industry publications. We believe that the surveys and market research others have performed are reliable, but we have not independently verified this information.

PROSPECTUS SUMMARY

The following summary highlights information contained elsewhere in this prospectus. This summary is not complete and does not contain all of the information that you should consider before investing in our common shares. You should read the entire prospectus, including “Risk Factors,” before making a decision to invest in our common shares. Unless the context suggests otherwise, references in this prospectus to “our company,” “we,” “us” and “our” mean Generation Income Properties, Inc. a Maryland real estate investment trust, and our consolidated subsidiaries, including Generation Income Properties, L.P., a Delaware limited partnership, the subsidiary through which we will conduct our business and which we refer to as our operating partnership, except where it is clear from the context that the term means only the issuer of the common shares, Generation Income Properties, Inc.

Our Company

We are an internally managed Maryland real estate investment trust (“REIT”) focused on acquiring and investing in net lease commercial retail, office and industrial properties located primarily in major cities in the United States. We were incorporated in June 2015, by our Chairman and President, David Sobelman, who has over 15 years of experience in the net lease real estate business and a successful track record operating two brokerage and advisory firms solely focused on net lease investments.

We intend to use substantially all of the net proceeds from this offering to acquire and operate a portfolio of commercial real estate consisting primarily of freestanding, single-tenant commercial properties. Because we did not identify any specific properties to purchase, prior to commencing our offering we are considered to be a blind pool.

As of the date of this offering circular we own one property and have one property under contract. On June 29, 2017, through a wholly owned subsidiary of our Operating Partnership, we purchased our first net lease asset with proceeds from the offering for $2,480,000 in cash plus closing costs. The property, on the ground floor of a new construction residential condominium building completed in 2016 is Unit 1A in the Quincy at Fourteenth Condominium at Quincy Street, NW, and 3707 14th Street, NW, Washington, D.C., it is located in the center of Washington D.C., approximately 3 miles north of the White House. Our tenant at this location is a corporate owned 7-Eleven convenience store. 7-Eleven, Inc. has an AA- credit rating from Standard & Poor’s.

On June 6, 2017, through our Operating Partnership, we entered into a contract to purchase a net lease property which completed construction in February 2018 in Tampa, FL. The free-standing, single tenant building was built to accommodate a Starbucks coffee. The property is located in the center of South Tampa in Tampa, FL and is located on a redeveloped property which replaces an approximately 50 year old building prior to construction of the new Starbucks building. Starbucks will operate and guarantee the 10-year lease (commencing upon the date that Starbucks is able to move into the location and begin operations). Starbucks has an A- credit rating from Standard & Poor’s. The purchase price is approximately $3,475,000 in cash plus closing costs and we expect to close on the property by the first quarter of 2018.

We have been organized and intend to operate in conformity with the requirements for qualification and taxation as a REIT under U.S. federal income tax laws, commencing with our taxable year ended December 31, 2018, and we expect to satisfy the requirements for qualification and taxation as a REIT under the U.S. federal income tax laws for our taxable year ending December 31, 2018, and subsequent taxable years.

[4]

Market Opportunity

We believe that there is a current trend to purchase U.S. net lease properties that provide the highest return possible, which in our estimation causes investors to purchase assets in less desirable locations with lower real estate values. In our estimation, this leaves an opportunity to purchase prime net lease real estate assets that are not being sought out by institutional owners. With the vast amount of similar REITs currently seeking assets that provide an immediate return, we believe that many assets are being overlooked. By contrast, we will be searching for assets that have a significant potential for long-term real estate appreciation, followed by a high credit rated tenant with a long-term, net lease. Other REITs, and even some private investors, are placing their investment focus on the initial return that is received when purchasing a specific property. Therefore, we believe that the market opportunity lies within uncovering assets that are overlooked by other institutional and private investors as they may not fit within their short-term higher return parameters.

Competitive Strengths

We expect the following factors will benefit our company as we implement our business strategy:

• | Experienced Leadership. We are led by our Chairman and President, David Sobelman. Mr. Sobelman has an extensive track record and substantial experience in the net lease industry. Mr. Sobelman founded 3 Properties, LLC, a Florida limited liability company, in 2017. 3 Properties is a multidisciplinary real estate brokerage and advisory firm focusing on net lease investments. Prior to 3 Properties, Mr. Sobelman co-founded Calkain Companies, LLC, a Virginia limited liability company. Calkain is a real estate firm also focusing exclusively on the net lease market. Mr. Sobelman wrote The Little Book of Triple Net Lease Investing, first and second editions, the first book ever written on the single tenant investment market as well as The Little Book on Urban Net Lease Investments, is a featured speaker at real estate conferences in the United States and abroad. Mr. Sobelman is also frequently quoted in The Wall Street Journal, Forbes, Fortune and various regional real estate trade publications. Mr. Sobelman regularly advises executive management of other real estate investment trusts and has moderated numerous conference panel discussions on REITs. Through his past professional experiences, Mr. Sobelman has developed an outstanding reputation in the net lease market as well as garnered strong relationships with net lease owners, management companies, brand companies, brokers, lenders and institutional and private investors, attorneys and accountants. |

|

|

• | Proven Acquirer with Strong Track Record of Growth. Throughout his career, Mr. Sobelman has helped acquire, redevelop, and reposition net lease properties. Mr. Sobelman has managed or overseen over 1,000 single-tenant net lease transactions and has been involved in about $10 billion in transactions during his tenure in the net lease real estate brokerage business. |

|

|

• | Focused Property Investment Strategy. We intend to invest primarily in assets that are geographically located in prime markets throughout the United States, with an emphasis on the major primary and coastal markets, where we believe there are greater barriers to entry for the development of new net lease properties. |

|

|

• | Prudent Capital Structure. We expect to maintain a low-leverage capital structure and intend to limit the sum of the outstanding principal amount of our consolidated indebtedness over the long-term. At this time we have no plans to issue any preferred stock. Our Board may modify or eliminate these limitations at any time without the approval of our shareholders. |

Business Strategy and Investment Criteria

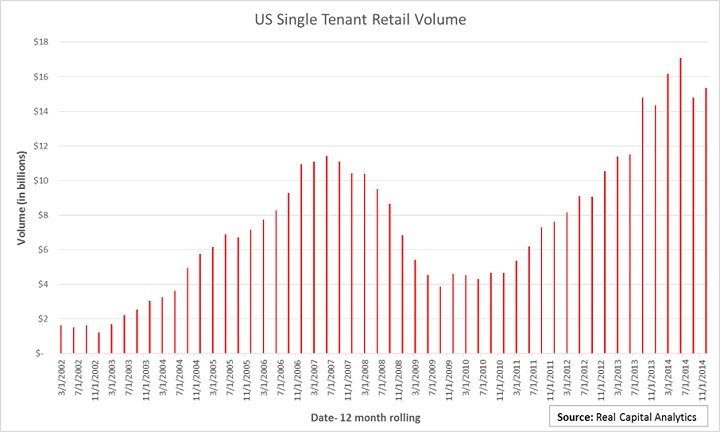

We intend to invest in net lease properties located primarily in major U.S. cities, with an emphasis on the major primary and coastal markets. We believe these markets have the most stable and predictable income and growth in value over a long period of time. We believe our target markets, including the coastal cities, are characterized by barriers to entry due to less supply of quality properties and that long-term real estate value and rental rate growth potential of net leases will likely continue to outperform the national average, as they have historically. According to research from Real Capital Analytics and our President’s industry knowledge, dense, infill real estate has historically proven to have increased, long-term real estate values as well as rental rate growth.

We will utilize extensive research to evaluate any target market and property, including a detailed review of the long-term economic outlook, trends in local demand generators, competitive environment, property systems and physical condition, and property financial performance. Specific acquisition criteria may include, but are not limited to, the following:

• | premier locations, facilities and other competitive advantages not easily replicated; |

|

|

• | barriers to entry in the market, such as scarcity of development sites, regulatory hurdles and long lead times for new development; |

[5]

• | potential return on investment initiatives, including redevelopment, improvements, and expansion; |

|

|

• | opportunities to implement value-added operational improvements; and |

|

|

• | strong demand growth characteristics supported by favorable demographic indicators. |

Initially, we do not intend to engage in significant development or redevelopment of net lease properties. However, we may engage in partial redevelopment and repositioning of certain properties, as we seek to maximize the financial performance of properties that we plan to acquire. In addition, we may acquire properties that require significant capital improvement, renovation or refurbishment.

Financing Strategies

Our anticipated long-term goal is to maintain a lower-leveraged capital structure. However, we anticipate in the early stages of our business, with respect to assets either acquired with debt financing or refinanced, the debt financing amount generally could be up to approximately 75% of the acquisition price of a particular asset; provided, however, we are not restricted in the amount of leverage we may use to finance an asset and certain assets may be more highly leveraged. Over time, we intend to reduce our debt positions through financing our long-term growth with equity issuances and some debt financing having staggered maturities. Our debt may include mortgage debt secured by our properties and unsecured debt. Over a long term period we intend to maintain lower levels of debt encumbering the REIT, its assets and/or the portfolio.

In June 2017, we received a $5,000,000 revolving line of credit from a commercial bank. We have not utilized any of our line of credit as of the date of this offering statement. The line is non-recourse and secured by the assets of GIP and matures in June 2019. We intend to repay amounts outstanding under any credit facilities as soon as reasonably possible. No assurance can be given that we will be able to obtain additional credit facilities. We anticipate utilizing this revolving credit facility to potentially fund future acquisitions (following investment of the net proceeds of this offering), return on investment initiatives and working capital requirements.

When purchasing net lease properties, we may issue limited partnership interests in our operating partnership as full or partial consideration to sellers who may desire to take advantage of tax deferral on the sale of a net lease or to participate in the potential appreciation in value of our common shares.

Executive Management Team

David Sobelman, our Chairman and President, founded us after working in the commercial real estate business for almost 15 years. Mr. Sobelman has held various roles within the single tenant, net lease commercial real estate investment market, including investor, asset manager, broker, owner, analyst and advisor. In 2017, Mr. Sobelman founded 3 Properties, LLC, a multidisciplinary real estate brokerage and advisory firm focused on net lease investments. Prior to founding 3 Properties, Mr. Sobelman in 2005, co-founded Calkain Companies, a real estate brokerage firm focused on net lease investments. During his tenure, Mr. Sobelman co-managed the company which grew from two employees to over 40 and 9 offices. Mr. Sobelman began his career in real estate in 2003 as an analyst at the firm of Grubb & Ellis, now Newmark Grubb Knight Frank, one of the largest commercial real estate advisory firms in the world. In 2000, Mr. Sobelman was appointed as the Confidential Aide to the U.S. Secretary of Health and Human Services and prior to this appointment; in 1998 he was a member of the Presidential advance team at the White House in Washington, D.C. During this time Mr. Sobelman was responsible for Presidential travel and logistics domestically and internationally. Mr. Sobelman wrote The Little Book of Triple Net Lease Investing, the first book ever written on the single tenant investment market, which is currently in its second edition. Mr. Sobelman as subsequently wrote his third book entitled The Little Book of Urban Net Lease Invesments. Mr. Sobelman is a featured speaker at conferences in the United States and abroad. Mr. Sobelman has been quoted or referred to in articles in The Wall Street Journal, Forbes, Fortune and various regional real estate trade publications.

Summary Risk Factors

An investment in our common shares involves various risks. You should carefully consider the matters discussed in “Risk Factors” beginning on page 12 of this prospectus before you decide whether to invest in our common shares. Some of the risks include the following:

• | Our president will face conflicts of interest, since he is our only executive officer and owns an interest in and serves as the managing member of 3 Properties, LLC, a real estate investment brokerage firm. We also may use 3 Properties, LLC as a brokerage agent in connection with assisting us to identify and purchase properties as well as the possibility of using 3 Properties, LLC for asset management. |

[6]

• | We may be subject to conflicts of interest arising out of our working with 3 Properties and their affiliates. Any of our agreements and arrangements with such parties, including those relating to compensation, payable by us to 3 Properties or its affiliates that may not be on terms that would result from arm’s-length negotiations between unaffiliated parties, and (2) conflicts related to compensation received by our sole-officer and director from 3 Properties. |

|

|

• | We currently have no employees and will initially rely on sole officer and directors and other paid outside consultants, lawyers and accountants until, due to our growth we need paid employees or an external management contract with fees. |

|

|

• | We have limited operating history, and limited capitalization. |

|

|

• | We only own one initial property and should not be considered diversified. We currently have one additional investment opportunity under contract, but investors will not have the opportunity to review investments to be made with our additional net proceeds prior to our making them. |

|

|

• | There is no assurance that we will be able to achieve our investment objectives; we may change our operational policies (including our investment objectives, strategies and policies) without stockholder consent at any time. |

|

|

• | This is considered a blind pool offering since we have not identified any properties to acquire, apart from one investment we have already made and one potential investment identified and under contract, with the proceeds of this offering,As a result, you will be unable to evaluate the economic merit of all of our future investments prior to our making them and there may be a substantial delay in receiving a return, if any, on your investment. |

|

|

• | You may not own more than 9.8% in value of the outstanding shares of our common stock or more than 9.8% of the number or value of any class or series of our outstanding shares of stock. Therefore, your ability to control the direction of our company will be limited. |

|

|

• | This is a best efforts offering and we might not sell all of the shares being offered. If we raise substantially less than the maximum offering, we may not be able to invest in a diverse portfolio of properties, and the value of your investment may vary more widely with the performance of specific properties. There is a greater risk that you will lose money in your investment if we cannot diversify our portfolio of investments by geographic location, tenant mix and lease terms. |

|

|

• | Our shares will not be listed at the time of purchase and you will have no immediate liquidity until such time as our shares are listed on a registered national securities exchange upon qualification or for quotation on the Over-The-Counter Bulletin Board (OTCBB) or OTC Markets Group OTCQB or OTCQX. |

|

|

• | If we fail to continue to qualify as a REIT for federal income tax purposes or if we qualify and subsequently lose our REIT status, our operations and ability to make distributions to our stockholders would be adversely affected. |

|

|

• | Our Board has the authority to designate and issue one or more classes or series of preferred stock without stockholder approval, with rights and preferences senior to the rights of holders of common stock, including rights to payment of distributions. If we issue any preferred shares, the amount of funds available for the payment of distributions on the common stock could be reduced or eliminated. |

|

|

• | Our shares should be considered as having only limited liquidity and at times may be illiquid. We are not required to provide a liquidity event to our shareholders. |

|

|

• | We may pay distributions from sources other than cash flow from operations, including, without limitation, the sale of assets, borrowings or offering proceeds. To the extent we pay distributions from sources other than our cash flows from operating activities, we may have less funds available for the acquisition of properties, and your overall return may be reduced. |

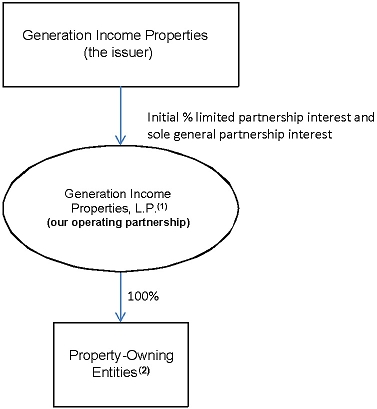

Our Organizational Structure

We were formed as a Maryland Corporation on June 19, 2015. We are the sole general partner of Generation Income Properties, L.P., the subsidiary through which we will conduct substantially all of our operations and make substantially all of our investments and which we refer to as our “Operating Partnership”. We will contribute to our Operating Partnership the net proceeds of this offering as our initial capital contribution in exchange for substantially all of the limited partnership interests in our Operating Partnership.

[7]

Because we will conduct substantially all of our operations through the Operating Partnership, we are considered an UPREIT. UPREIT stands for “Umbrella Partnership Real Estate Investment Trust.” We use an UPREIT structure because a sale of property directly to a REIT generally is a taxable transaction to the selling property owner. In an UPREIT structure, a seller of a property that desires to defer taxable gain on the sale of its property may transfer the property to the UPREIT in exchange for limited partnership units in the UPREIT and defer taxation of gain until the seller later exchanges its UPREIT units on a one-for-one basis for REIT shares. If the REIT shares are publicly traded, at the time of the exchange of units for shares, the former property owner will achieve liquidity for its investment. Using an UPREIT structure may give us an advantage in acquiring desired properties from persons who may not otherwise sell their properties because of unfavorable tax results.

In the future we may issue limited partnership interests in our Operating Partnership as consideration for the purchase of net lease properties or in connection with an equity incentive plan.

The following chart shows the current structure of our company:

(1) | Upon completion of this offering, we will issue an aggregate of 200,000 LTIP units to Mr. Sobelman, our sole officer and director. |

|

|

(2) | As of the date of this offering statement the Company has formed two Property-Owning Entities GIPDC 3707 14th Street, LLC and GIPFL 1300 S Dale Mabry, LLC. Each of the Property-Owning Entities is 100% owned and operated by our Operating Partnership. |

Tax Status

We intend to elect to be taxed as a REIT for federal income tax purposes commencing with our taxable year ending on December 31, 2018. Our qualification as a REIT will depend upon our ability to meet, on a continuing basis, through actual investment and operating results, various complex requirements under the Internal Revenue Code of 1986, as amended (“the Code”) relating to, among other things, the sources of our gross income, the composition and values of our assets, our distribution levels and the diversity of ownership of our shares. We believe that we will be organized in conformity with the requirements for qualification as a REIT under the Code and that our intended manner of operation will enable us to meet the requirements for qualification and taxation as a REIT for federal income tax purposes commencing with our taxable year ending December 31, 2018 and continuing thereafter.

[8]

As a REIT, we generally will not be subject to federal income tax on our REIT taxable income that we distribute currently to our shareholders. Under the Code, REITs are subject to numerous organizational and operational requirements, including a requirement that they distribute each year at least 90% of their taxable income, determined without regard to the deduction for dividends paid and excluding any net capital gains. If we fail to qualify for taxation as a REIT in any taxable year and do not qualify for certain statutory relief provisions, our income for that year will be taxed at regular corporate rates, and we will be disqualified from taxation as a REIT for the four taxable years following the year during which we ceased to qualify as a REIT. Even if we qualify as a REIT for federal income tax purposes, we may still be subject to state and local taxes on our income and assets and to federal income and excise taxes on our undistributed income.

Distribution Policy

We intend to make distributions consistent with our intent to be taxed as a REIT under the Code. We intend to make regular quarterly distributions to our shareholders beginning at such time as our board of directors (“Board”) determines that we have acquired properties generating sufficient cash flow to do so. Until we invest a substantial portion of the net proceeds of this offering, we expect our distributions will be nominal. We cannot predict the timing of our investments or when we will commence paying quarterly distributions.

In order to qualify for taxation as a REIT, we intend to make annual distributions to our shareholders of at least 90% of our taxable income, determined without regard to the deduction for dividends paid and excluding any net capital gains. We cannot assure you as to when we will begin to generate sufficient cash flow to make distributions to our shareholders or our ability to sustain those distributions. Distributions will be authorized by our Board and declared by us based upon a variety of factors deemed relevant by our directors. Distributions to our shareholders out of our earnings and profits generally will be taxable to our shareholders as ordinary income.

Restrictions on Ownership of Our Common Shares

Due to limitations on the concentration of ownership of REIT stock imposed by the Code, our charter generally prohibits any person from actually, beneficially or constructively owning more than 9.8% in value or number of shares, whichever is more restrictive, of the outstanding shares of our common stock or more than 9.8% in value of the aggregate outstanding shares of all classes and series of our stock (the “Ownership Limits”).

THE OFFERING

Common Stock Offered: | 4,000,000 shares |

Common Stock outstanding before this Offering: | 1,000,000 |

Common Stock to be Outstanding after this Offering: | 5,000,000 common shares will be issued and outstanding if we sell all of the shares in this offering. |

The minimum number of Common Stock to be sold in this Offering: | None |

Price per Share: | $5.00 |

Market for the Common Stock | There is no public market for the common shares. We may not be able to meet the requirement for a public listing or quotation of our common stock. Further, even if our common stock is quoted or granted listing, a market for the common shares may not develop. The offering price for the shares will remain $5 per share for the duration of the offering. |

[9]

Use of Proceeds: | We will receive all proceeds from the sale of the Common Stock. We intend to contribute the net proceeds of this offering, minus the costs associated with this offering, to our operating partnership. Our operating partnership will invest these net proceeds in net lease properties in accordance with our investment strategy described in this prospectus and for general business purposes. We will use approximately $100,000 of the proceeds to reimburse Mr. Sobelman for the legal, accounting, and sales and marketing expenses he incurred on our behalf in connection with the formation of our company and this offering. |

Selling Securityholders: | There are no selling securityholders in this offering. |

Risk Factors: | Investing in our common stock involves risks. You should carefully read and consider the information set forth under the heading “Risk Factors” beginning on page 12 and other information included in this prospectus before investing in our common stock. |

Termination Date | We currently expect that this offering shall remain open until the date when the sale of all 4,000,000 shares is completed; provided, however, the offering shall terminate by May 1, 2018. We reserve the right to terminate this offering for any reason at any time. |

Tier 2 Offering under Regulation A+

This is a Regulation A+ Tier 2 offering where the securities will not be listed on a registered national securities exchange upon qualification. However, we intend to apply for our common stock to become eligible for quotation on the OTC through the OTCBB, the OTCQX or the OTCQB upon the termination of this offering. There is no guarantee that we will be quoted or listed or that a market will develop.

Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

Emerging Growth Company

The Jumpstart Our Business Startups Act, or the JOBS Act, was enacted in April 2012 with the intention of encouraging capital formation in the United States and reducing the regulatory burden on newly public companies that qualify as “Emerging Growth Companies.” We meet the definition of an emerging growth company within the meaning of the JOBS Act. As an emerging growth company, we may take advantage of certain exemptions from various public reporting requirements and so long as we qualify as an emerging growth company, we will, among other things:

• | be temporarily exempted from the internal control audit requirements under Section 404(b) of the Sarbanes-Oxley Act; |

|

|

• | be temporarily exempted from various existing and forthcoming executive compensation-related disclosures, for example: “say-on-pay”, “pay-for-performance”, and “CEO pay ratio”; |

|

|

• | be temporarily exempted from any rules that might be adopted by the Public Company Accounting Oversight Board requiring mandatory audit firm rotation or supplemental auditor discussion and analysis reporting; |

|

|

• | be temporarily exempted from having to solicit advisory say-on-pay, say-on-frequency and say-on-golden-parachute shareholder votes on executive compensation under Section 14A of the Securities Exchange Act of 1934, as amended; |

|

|

• | be permitted to comply with the SEC’s detailed executive compensation disclosure requirements on the same basis as a smaller reporting company; and |

|

|

• | be permitted to use any extended transition periods allowed by new or revised accounting standards that have different effective dates for public and private companies. |

[10]

We will continue to be an emerging growth company until the earliest of:

• | the last day of the fiscal year during which we have annual total gross revenues of $1 billion or more; |

|

|

• | the last day of the fiscal year following the fifth anniversary of the first sale of our common equity securities in an offering registered under the Securities Act; |

|

|

• | the date on which we issue more than $1 billion in non-convertible debt securities during a previous three-year period; or |

|

|

• | the date on which we become a large accelerated filer, which generally is a company with a public float of at least $700 million (Exchange Act Rule 12b-2). |

Section 107 of the JOBS Act provides that an emerging growth company can elect to take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We intend to take advantage of the extend transition period provided under Section 107 of the JOBS Act.

Our Information

We were incorporated in Maryland on June 19, 2015. Our business and registered office is located at 401 East Jackson Street, Suite 3300, Tampa, Florida 33602. Our office space has been provided free of charge by David Sobelman, our sole director and officer. Our telephone number is (813) 448-1234; our main email address is: ds@gipreit.com.

RISK FACTORS

An investment in our common shares involves risks. In addition to other information in this prospectus, you should carefully consider the following risks before investing in our common shares offered by this prospectus. The occurrence of any of the following risks could materially and adversely affect our business, prospects, financial condition, results of operations and our ability to make cash distributions to our shareholders, which could cause you to lose all or a significant portion of your investment in our common shares. Some statements in this prospectus, including statements in the following risk factors, constitute forward-looking statements.

Risks Related To Our Financial Condition

Because there is no required minimum proceeds we can receive from this offering, the company may not raise sufficient capital to implement its planned business and your entire investment could be lost.

This offering is being made on a best-efforts basis and there is no minimum amount of proceeds we may receive and all funds raised regardless of the amount will be available to us. In the event that we do not raise sufficient capital to implement our planned operations, your entire investment could be lost.

We have not generated any profit to date and have incurred primarily losses since inception.

We generated no revenues as of December 31, 2016 and we have cumulative net losses of approximately $285,650 from inception to December 31, 2016. As of the date of this offering statement we’ve generated approximately $100,000 in revenue attributed to rental income from our first investment.

Risks Related To This Offering

We are selling shares in this offering without using the traditional services of an underwriter, and there is a risk that we will be unable to sell the shares we are offering.

This offering is a self-underwritten offering, and therefore there is no guarantee that we will sell all or any part of the shares offered in this offering. We will require additional funding to continue our business, and there is no assurance that we will be able to locate additional funding.

[11]

Because there is no public trading market for our common stock, you may not be able to resell your stock.

We intend to apply for quotation of our common stock quoted on the OTC through the OTCBB, OTCQX, or OTCQB. This process takes at least 60 days and the application must be made on our behalf by a market maker. Our stock may be listed or traded only to the extent that there is interest by broker-dealers in acting as a market maker. Despite our best efforts, we may not be able to convince any broker/dealers to act as market-makers and make quotations on the OTC. We may consider pursuing a listing on the OTCBB, OTCQB or OTCQX after this registration becomes effective and we have completed our offering.

If our common stock becomes listed and a market for the stock develops, the actual price of our shares will be determined by prevailing market prices at the time of the sale. We cannot assure you that there will be a market in the future for our common stock. The trading of securities on the OTC is often sporadic and investors may have difficulty buying and selling our shares or obtaining market quotations for them, which may have a negative effect on the market price of our common stock. You may not be able to sell your shares at their purchase price or at any price at all.

Investing in our company may result in an immediate loss because buyers may pay more for our common stock than the pro rata portion of the assets are worth.

We have only a limited operating history with nominal earnings; therefore, the price of the offered shares is not based on any data. The offering price and other terms and conditions regarding our shares have been arbitrarily determined and do not bear any relationship to assets, earnings, book value or any other objective criteria of value. No investment banker, appraiser or other independent third party has been consulted concerning the offering price for the shares or the fairness of the offering price used for the shares. The offering price will not change for the duration of the offering even if we obtain a listing on any exchange or become quoted on the OTCBB, OTCQX or OTCQB. The Company’s sole officer and director paid $.01 per share, a difference of $4.99 per share lower than the share price in this offering.

Because we have 110,000,000 authorized shares of stock, management could issue additional shares, diluting the current shareholders’ equity.

We have 100,000,000 authorized shares of common stock and 10,000,000 authorized shares of preferred stock, of which only 1,000,000 shares of common stock are currently issued and outstanding and if all the shares offered are sold in this offering, then only 5,000,000 shares of common stock will be issued and outstanding after this offering terminates. Our management could, without the consent of the existing shareholders, issue substantially more shares of common stock, causing a large dilution in the equity position of our current shareholders. Additionally, large share issuances would generally have a negative impact on our share price. It is possible that, due to additional share issuance, you could lose a substantial amount, or all, of your investment.

In the event that our shares are traded, they may trade under $5.00 per share and thus will be a penny stock. Trading in penny stocks has many restrictions and these restrictions could severely affect the price and liquidity of our shares.

In the event that our shares are traded, and our stock trades below $5.00 per share, our stock would be known as a “penny stock”, which is subject to various regulations involving disclosures to be given to you prior to the purchase of any penny stock. The U.S. Securities and Exchange Commission (the “SEC”) has adopted regulations which generally define a “penny stock” to be any equity security that has a market price of less than $5.00 per share, subject to certain exceptions. Depending on market fluctuations, our common stock could be considered to be a “penny stock”. A penny stock is subject to rules that impose additional sales practice requirements on broker/dealers who sell these securities to persons other than established customers and accredited investors. For transactions covered by these rules, the broker/dealer must make a special suitability determination for the purchase of these securities.

In addition, he must receive the purchaser’s written consent to the transaction prior to the purchase. He must also provide certain written disclosures to the purchaser. Consequently, the “penny stock” rules may restrict the ability of broker/dealers to sell our securities, and may negatively affect the ability of holders of shares of our common stock to resell them. These disclosures require you to acknowledge that you understand the risks associated with buying penny stocks and that you can absorb the loss of your entire investment. Penny stocks are low priced securities that do not have a very high trading volume. Consequently, the price of the stock is often volatile and you may not be able to buy or sell the stock when you want to.

[12]

An investment in our shares will have limited liquidity and we are not required, through our charter or otherwise, to provide for a liquidity event.

We cannot guarantee that a liquidity event will occur. Our shares will not be listed at the time of purchase and you will have no immediate liquidity until such time as our shares are listed, if at all, on a registered national securities exchange upon qualification or for quotation on the Over-The-Counter market. In addition, we are not obligated, through our charter or otherwise, to effectuate a liquidity event and may not effect a liquidity event. If we do not effect a liquidity event, it will be very difficult for you to have liquidity for your investment in the shares of our common stock.

As we may be unable to create or sustain a market for the company’s shares, they may be extremely illiquid.

If no market develops, the holders of our common stock may find it difficult or impossible to sell their shares. Further, even if a market develops, our common stock will be subject to fluctuations and volatility and we cannot apply directly to be quoted on the Over-The-Counter market (OTC). Additionally, the stock may be quoted or traded only to the extent that there is interest by broker-dealers in acting as a market maker in our stock. Despite our best efforts, we may not be able to convince any broker/dealers to act as market-makers and make quotations on any of the OTCBB, OTCQX or OTCQB.

The amount of distributions we may pay, if any, is uncertain. We may pay distributions from sources other than our cash flow from operations, including, borrowings or offering proceeds.

We may pay distributions from sources other than from our cash flow from operations. We intend to fund the payment of regular distributions to our stockholders entirely from cash flow from our operations. However, during the early stages of our operations, and from time to time thereafter, we may not generate sufficient cash flow from operations to fully fund distributions to stockholders. Therefore, particularly in the earlier part of this offering, if we choose to pay a distribution, we may choose to use cash flows from financing activities, which include borrowings (including borrowings secured by our assets), net proceeds of this offering, or other sources to fund distributions to our stockholders. To the extent that we fund distributions from sources other than cash flows from operations, shareholders may experience further dilution in their investment.

We have not adopted a stock redemption program, so you may be unable to recover your investment.

We have not adopted a stock redemption plan to provide a means for liquidity. Given our relatively small size, it is highly unlikely that a redemption plan would be developed within the foreseeable future. In addition, even if we adopted a redemption plan, we would have discretion to not redeem your shares, to suspend the plan and to cease redemptions. Currently, there is no public market for the shares, so stockholders may be unable to sell their shares or may only be able to sell their shares at an undesirable discounted price or after considerable delay.

Financial Industry Regulatory Authority (“FINRA”) sales practice requirements may also limit your ability to buy and sell our common stock, which could depress the price of our shares.

We intend to apply for quotation of our common stock quoted on the OTC Bulletin Board “OTCBB” or through the OTC Markets Group “OTCQX” “OTCQB” at which time we will be subject to FINRA rules which require broker-dealers to have reasonable grounds for believing that an investment is suitable for a customer before recommending that investment to the customer. Prior to recommending speculative low-priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer’s financial status, tax status and investment objectives, among other things. Under interpretations of these rules, FINRA believes that there is a high probability such speculative low-priced securities will not be suitable for at least some customers. Thus, FINRA requirements make it more difficult for broker-dealers to recommend that their customers buy our common stock, which may limit your ability to buy and sell our shares, have an adverse effect on the market for our shares, and thereby depress our share price.

You may face significant restrictions on the resale of your shares due to state “blue sky” laws.

Each state has its own securities laws, often called “blue sky” laws, which (1) limit sales of securities to a state’s residents unless the securities are registered in that state or qualify for an exemption from registration, and (2) govern the reporting requirements for broker-dealers doing business directly or indirectly in the state. Before a security is sold in a state, there must be a registration in place to cover the transaction, or it must be exempt from registration. The applicable broker-dealer must also be registered in that state.

[13]

We do not know whether our securities will be registered or exempt from registration under the laws of any state. A determination regarding registration will be made by those broker-dealers, if any, who agree to serve as market makers for our common stock. We have not yet applied to have our securities registered in any state and will not do so until we receive expressions of interest from investors in specific states after they have viewed this Prospectus. There may be significant state blue sky law restrictions on the ability of investors to sell, and on purchasers to buy, our securities. You should therefore consider the resale market for our common stock to be limited, as you may be unable to resell your shares without the significant expense of state registration or qualification.

Risks Related to our Common Stock And Structure

Any additional funding we arrange through the sale of our common stock will result in dilution to existing stockholders.

We may have to raise additional capital in order for our business plan to succeed. Our most likely source of additional capital will be through the sale of additional shares of common stock. Such stock issuances will cause stockholders’ interests in our company to be diluted. Such dilution will negatively affect the value of an investor’s shares.

Risks Related to Our Business and Properties

The limits on the percentage of shares of our common stock that any person may own may discourage a takeover or business combination that could otherwise benefit our stockholders.

Our charter, with certain exceptions, authorizes our Board to take such actions as are necessary and desirable to preserve our qualification as a REIT. Unless exempted by our Board, no person may own more than 9.8% in value of our outstanding capital stock or more than 9.8% in value or number of shares, whichever is more restrictive, of our outstanding common stock. A person that did not acquire more than 9.8% of our shares may become subject to our charter restrictions if redemptions by other stockholders cause such person’s holdings to exceed 9.8% of our outstanding shares. Our 9.8% ownership limitation may have the effect of delaying, deferring or preventing a change in control of us, including an extraordinary transaction (such as a merger, tender offer or sale of all or substantially all of our assets) that might provide a premium price for our stockholders.

Our charter permits our board of directors to issue stock with terms that may subordinate the rights of the holders of our common stock or discourage a third party from acquiring us in a manner that could result in a premium price to our stockholders.

Our Board may classify or reclassify any unissued common stock or preferred stock into other classes or series of stock and establish the preferences, conversion or other rights, voting powers, restrictions, limitations as to dividends and other distributions, qualifications and terms or conditions of redemption of any such stock without stockholder approval. Thus, our Board could authorize the issuance of preferred stock with terms and conditions that could have priority as to distributions and amounts payable upon liquidation over the rights of the holders of our common stock. Such preferred stock could also have the effect of delaying, deferring or preventing a change in control of us, including an extraordinary transaction (such as a merger, tender offer or sale of all or substantially all of our assets) that might otherwise provide a premium price to holders of our common stock.

Maryland law and our organizational documents limit our rights and the rights of our stockholders to recover claims against our directors and officers, which could reduce your and our recovery against them if they cause us to incur losses.

Maryland law provides that a director will not have any liability as a director so long as he or she performs his or her duties in accordance with the applicable standard of conduct. In addition, Maryland law and our charter provide that no director or officer shall be liable to us or our stockholders for monetary damages unless the director or officer (1) actually received an improper benefit or profit in money, property or services or (2) was actively and deliberately dishonest as established by a final judgment as material to the cause of action. Moreover, our charter generally requires us to indemnify and advance expenses to our directors and officers for losses they may incur by reason of their service in those capacities unless their act or omission was material to the matter giving rise to the proceeding and was committed in bad faith or was the result of active and deliberate dishonesty, they actually received an improper personal benefit in money, property or services or, in the case of any criminal proceeding, they had reasonable cause to believe the act or omission was unlawful. Further, we have entered into separate indemnification agreements with each of our officers and directors. As a result, you and we may have more limited rights against our directors or officers than might otherwise exist under common law, which could reduce your and our recovery from these persons if they act in a manner that causes us to incur losses. In addition, we are obligated to fund the defense costs incurred by these persons in some cases.

[14]

Certain provisions of Maryland law could inhibit transactions or changes of control under circumstances that could otherwise provide stockholders with the opportunity to realize a premium.

Certain provisions of the Maryland General Corporation Law applicable to us prohibit business combinations with: (1) any person who beneficially owns 10% or more of the voting power of our outstanding voting stock, which we refer to as an “interested stockholder;” (2) an affiliate or associate of ours who, at any time within the two-year period prior to the date in question, was the beneficial owner of 10% or more of the voting power of our then outstanding stock, which we also refer to as an “interested stockholder;” or (3) an affiliate of an interested stockholder. These prohibitions last for five years after the most recent date on which the interested stockholder became an interested stockholder. Thereafter, any business combination with the interested stockholder or an affiliate of the interested stockholder must be recommended by our Board and approved by the affirmative vote of at least 80% of the votes entitled to be cast by holders of our outstanding voting stock, and two-thirds of the votes entitled to be cast by holders of our voting stock other than shares held by the interested stockholder or its affiliate with whom the business combination is to be effected or held by an affiliate or associate of the interested stockholder. These requirements could have the effect of inhibiting a change in control even if a change in control were in our stockholders’ best interest. These provisions of Maryland law do not apply, however, to business combinations that are approved or exempted by our Board prior to the time that someone becomes an interested stockholder. Pursuant to the business combination statute, our Board has exempted any business combination involving us and any person, provided that such business combination is first approved by a majority of our Board.

Our UPREIT structure may result in potential conflicts of interest with limited partners in our operating partnership whose interests may not be aligned with those of our stockholders.

Our directors and officers have duties to our corporation and our stockholders under Maryland law and our charter in connection with their management of the corporation. At the same time, we, as general partner, will have fiduciary duties under Delaware law to our operating partnership and to the limited partners in connection with the management of our operating partnership. Our duties as general partner of our operating partnership and its partners may come into conflict with the duties of our directors and officers to our corporation and our stockholders. Under Delaware law, a general partner of a Delaware limited partnership owes its limited partners the duties of good faith and fair dealing. Other duties, including fiduciary duties, may be modified or eliminated in the partnership’s partnership agreement. The partnership agreement of our operating partnership provides that, for so long as we own a controlling interest in our operating partnership, any conflict that cannot be resolved in a manner not adverse to either our stockholders or the limited partners will be resolved in favor of our stockholders.

Additionally, the partnership agreement expressly limits our liability by providing that we will not be liable or accountable to our operating partnership for losses sustained, liabilities incurred or benefits not derived if we acted in good faith. In addition, our operating partnership is required to indemnify us and our officers, directors, employees, agents and designees to the extent permitted by applicable law from and against any and all claims arising from operations of our operating partnership, unless it is established that: (1) the act or omission was material to the matter giving rise to the proceeding and either was committed in bad faith or was the result of active and deliberate dishonesty; (2) the indemnified party received an improper personal benefit in money, property or services; or (3) in the case of a criminal proceeding, the indemnified person had reasonable cause to believe that the act or omission was unlawful.

The provisions of Delaware law that allow the fiduciary duties of a general partner to be modified by a partnership agreement have not been tested in a court of law, and we have not obtained an opinion of counsel covering the provisions set forth in the partnership agreement that purport to waive or restrict our fiduciary duties.

We have limited operating history and may not be able to successfully operate our business or generate sufficient operating cash flows to make or sustain distributions to our shareholders.

We were organized in June 2015 for the purpose of engaging in the activities set forth in this offering circular, we achieved an initial closing and acquired our first property in June 2017 and have one agreement to acquire our second net lease property. Therefore, we have limited operating history We commenced operations as soon as were able to raise sufficient funds to acquire our first suitable property because there is no minimum amount that we must raise. However, our ability to make or sustain distributions to our shareholders will depend on many factors, including our availability to identify attractive acquisition opportunities that satisfy our investment strategy, our success in consummating acquisitions on favorable terms, the level and volatility of interest rates, readily accessible short-term and long-term financing on favorable terms, and conditions in the financial markets, the real estate market and the economy. We will face competition in acquiring attractive net lease properties. The value of the net lease properties that we acquire may decline substantially after we purchase them. We may not be able to successfully operate our business or implement our operating policies and investment strategy successfully. Furthermore, we may not be able to generate sufficient operating cash flow to pay our operating expenses and make distributions to our shareholders.

[15]

As an early stage company , we are subject to the risks of any early stage business enterprise, including risks that we will be unable to attract and retain qualified personnel, create effective operating and financial controls and systems or effectively manage our anticipated growth, any of which could have a harmful effect on our business and our operating results.

We may change our investment objectives without seeking stockholder approval.

We may change our investment objectives without shareholder notice or consent. Although our Board has fiduciary duties to our stockholders and intends only to change our investment objectives when our Board determines that a change is in the best interests of our stockholders, a change in our investment objectives could reduce our payment of cash distributions to our stockholders or cause a decline in the value of our investments.

We only own one net lease property and have only identified one net lease property to acquire and you will be unable to evaluate the allocation of net proceeds of this offering or the economic merits of our investments prior to making your investment decision.

Since we have not yet identified all the net lease properties to acquire or committed the net proceeds of this offering to any specific net lease property investment other than the property we acquired in June 2017 and the property we have under agreement to acquire in the first quarter of 2018, you will be unable to evaluate the allocation of the net proceeds or the economic merits of our acquisitions before making an investment decision to purchase our common shares. As a result, we will have broad authority to invest the net proceeds in any real estate investments that we may identify in the future and we may use those proceeds to make investments with which you may not agree. In addition, our investment policies may be amended or revised from time to time at the discretion of our Board, without a vote of our shareholders. These factors will increase the uncertainty, and thus the risk, of investing in our common shares. Our failure to apply the net proceeds effectively or find suitable net lease properties to acquire in a timely manner or on acceptable terms could result in returns that are substantially below expectations or result in losses. Prior to the full investment of the net offering proceeds in net lease properties, we intend to invest the net proceeds in interest-bearing short-term, investment grade securities or money-market accounts which are consistent with our intention to qualify as a REIT. These investments are expected to provide a lower net return than we will seek to achieve from our investments in net lease properties. We may not be able to identify net lease investments that meet our investment criteria, we may not be successful in completing any investment we identify and our investments may not produce acceptable, or any, returns. We may be unable to invest the proceeds on acceptable terms, or at all.

Our sole officer and director devotes some of his business time to other activities and may not be in a position to devote his full time to our operations, which may result in periodic interruptions and even business failure.

Mr. Sobelman, our sole officer and director, has other outside business activities and intends to devote approximately 10-25 hours per week to our operations. Our operations may be sporadic and occur at times which are not convenient to Mr. Sobelman, which may result in periodic interruptions or suspensions of our plans to acquire properties and begin generating revenues. Such delays could have a significant negative effect on the success of the business.

We plan to use outside consultants, attorneys, and accountants, as necessary and do not plan to engage any additional full-time employees in the near future.

Our sole officer and director may leave employment with us, which could adversely affect our ability to continue operations.

Because we are entirely dependent on the efforts of our sole officer and director, his departure and our inability to find suitable replacement, or the loss of other key personnel in the future, could have a harmful effect on the business.

There is currently no agreement in writing between us and Mr. Sobelman, which means that there is no means to guarantee that he will stay working with us.

There may be conflicts of interest faced by our sole officer and director, who is also a managing partner in 3 Properties, which may compete with us for his business time and for business opportunities to acquire properties that may arise.

Mr. Sobelman, our sole officer and director, is also the managing member of 3 Properties, which is a business formed in 2017 that operates as a commercial real estate broker. We may compete for Mr. Sobelman’s time. We do not have an employment agreement with Mr. Sobelman to provide services or to present business opportunities to us. Moreover, he has obligations toward 3 Properties for his business time and existing fiduciary duties to that entity. Thus, if Mr. Sobelman does not devote sufficient time to us, or we are unable to obtain business opportunities to acquire properties sufficient for us to generate revenues, then our business may not succeed.

[16]

Because our sole officer and director will have broad discretion to invest the net proceeds of this offering he may make investments where the returns are substantially below expectations or which result in net operating losses.

Our sole officer and director will have broad discretion, within the general investment criteria established by our Board, to invest the net proceeds of this offering and to determine the timing of such investments. In addition, our investment policies may be revised from time to time at the discretion of our Board, without a vote of our shareholders. Such discretion could result in investments that may not yield returns consistent with expectations.

We and our third party vendors will rely on information technology networks and systems in providing services to us, and any material failure, inadequacy, interruption or security failure of that technology could harm our business.

We and our third party vendors will rely on information technology networks and systems, including the Internet, to process, transmit and store electronic information and to manage or support a variety of our business processes, including financial transactions and maintenance of records, which may include confidential information of tenants, lease data and information regarding our stockholders. We and our third party vendors will rely on commercially available systems, software, tools and monitoring to provide security for processing, transmitting and storing confidential information. Security breaches, including physical or electronic break-ins, computer viruses, attacks by hackers and similar breaches or cyber-attacks, can create system disruptions, shutdowns or unauthorized disclosure of confidential information. In addition, any breach in the data security measures employed by the third party vendors upon which we rely, could also result in the improper disclosure of personally identifiable information. Any failure to maintain proper function, security and availability of information systems could interrupt our operations, damage our reputation, subject us to liability claims or regulatory penalties and could materially and adversely affect us.

General Risks Related to Investments in Real Estate

Our operating results will be affected by economic and regulatory changes that have an adverse impact on the real estate market in general, and we cannot assure you that we will be profitable or that we will realize growth in the value of our real estate properties.

Our operating results are subject to risks generally incident to the ownership of real estate, including:

| • | ability to acquire properties: |

|

|

|

| • | changes in general economic or local conditions; |

|

|

|

| • | changes in supply of or demand for similar or competing properties in an area; |

|

|

|

| • | changes in interest rates and availability of permanent mortgage funds that may render the sale of a property difficult or unattractive; |

|

|

|

| • | changes in tax, real estate, environmental and zoning laws; and |

|

|

|

| • | periods of high interest rates and tight money supply. |

These and other reasons may prevent us from being profitable or from realizing growth or maintaining the value of our real estate properties.

We currently only own one property to lease, which generates limited source of revenue. Without funds from this offering, we will face difficulty acquiring any properties to lease to generate revenue. Many of our future properties will likely depend upon a single tenant for all or a majority of their rental income, and our financial condition and ability to make distributions may be adversely affected by the bankruptcy or insolvency, a downturn in the business, or a lease termination of a single tenant.

We currently only own one property to lease to tenants and need to raise funds to acquire additional such properties. We expect that many of our properties will be occupied by only one tenant or will derive a majority of their rental income from one tenant and, therefore, the success of those properties will be materially dependent on the financial stability of such tenants. Lease payment defaults by tenants could cause us to reduce the amount of distributions we pay. A default of a tenant on its lease payments to us would cause us to lose the revenue from the property and force us to find an alternative source of revenue to meet any mortgage

[17]

payment and prevent a foreclosure if the property is subject to a mortgage. In the event of a default, we may experience delays in enforcing our rights as landlord and may incur substantial costs in protecting our investment and re-letting the property. If a lease is terminated, there is no assurance that we will be able to lease the property for the rent previously received or sell the property without incurring a loss. A default by a tenant, the failure of a guarantor to fulfill its obligations or other premature termination of a lease, or a tenant’s election not to extend a lease upon its expiration, could have an adverse effect on our financial condition and our ability to pay distributions.

We may be subject to conflicts of interest arising out of our working with 3 Properties, , a company managed by our sole officer and director.

We may purchase properties where 3 Properties identifies properties for the Company or represents the seller of a property we purchase. A conflict of interest may exist in such an acquisition since 3 Properties may be entitled to a real estate brokerage commission in connection to such a transaction. Any of our agreements and arrangements with 3 Properties, including those relating to compensation, are not the result of arm’s length negotiations.

If a major tenant declares bankruptcy, we may be unable to collect balances due under relevant leases, which could have a harmful effect on our financial condition and ability to pay distributions to you.

Our success will depend on the financial ability of our eventual tenants to remain current with their leases with us. We may experience concentration in one or more tenants if the future leases we have with those tenants represent a significant percentage of our operations. Any of our future tenants, or any guarantor of one of our future tenant’s lease obligations, could be subject to a bankruptcy proceeding pursuant to Title 11 of the bankruptcy laws of the United States. Such a bankruptcy filing would bar us from attempting to collect pre-bankruptcy debts from the bankrupt tenant or its properties unless we receive an enabling order from the bankruptcy court. Post-bankruptcy debts would be paid currently. If we assume a lease, all pre-bankruptcy balances owing under it must be paid in full. If a lease is rejected by a tenant in bankruptcy, we would have a general unsecured claim for damages. This claim could be paid only in the event funds were available, and then only in the same percentage as that realized on other unsecured claims.