UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 1-K

ANNUAL REPORT PURSUANT TO REGULATION A OF THE SECURITIES ACT OF 1933

For the fiscal year ended December 31, 2020

GENERATION INCOME PROPERTIES, INC.

(Exact name of registrant as specified in its charter)

Commission File Number: 24R-00019

Maryland | 47-4427295 |

(State or other jurisdiction of | (I.R.S. Employer |

|

|

401 East Jackson Street | 33602 |

(813)-448-1234

Registrant’s telephone number, including area code

Common Stock, $0.01 par value per share

(Title of each class of securities issued pursuant to Regulation A)

Part II.

STATEMENTS REGARDING FORWARD-LOOKING INFORMATION

We make statements in this Annual Report pursuant to Regulation A on Form 1-K (the “Annual Report”) that are forward-looking statements within the meaning of the federal securities laws. The words “believe,” “estimate,” “expect,” “anticipate,” “intend,” “plan,” “seek,” “may,” “continue,” “could,” “might,” “potential,” “predict,” “should,” “will,” “would,” and similar expressions or statements regarding future periods or the negative of these terms are intended to identify forward-looking statements. These forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause our actual results, performance or achievements, or industry results, to differ materially from any predictions of future results, performance or achievements that we express or imply in this Annual Report or in the information incorporated by reference into this Annual Report.

The forward-looking statements included in this Annual Report are based upon our current expectations, plans, estimates, assumptions and beliefs that involve numerous risks and uncertainties. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond our control. Although we believe that the expectations reflected in such forward-looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth in the forward-looking statements. Since our common stock may be considered a “penny stock,” we may be ineligible to rely on the safe harbor for forward-looking statements provided in Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities and Exchange Act of 1934, as amended (the “Exchange Act”).

Factors that could have a material adverse effect on our forward-looking statements and upon our business, results of operations, financial condition, funds derived from operations, cash available for distribution, cash flows, liquidity and prospects include, but are not limited to, the factors in this Annual Report under the caption “RISK FACTORS.”

Any of the assumptions underlying forward-looking statements could be inaccurate. You are cautioned not to place undue reliance on any forward-looking statements included in this Annual Report. All forward-looking statements are made as of the date of this Annual Report and the risk that actual results will differ materially from the expectations expressed in this Annual Report will increase with the passage of time. Except as otherwise required by the federal securities laws, we undertake no obligation to publicly update or revise any forward-looking statements after the date of this Annual Report, whether as a result of new information, future events, changed circumstances or any other reason. In light of the significant uncertainties inherent in the forward-looking statements included in this Annual Report, the inclusion of such forward-looking statements should not be regarded as a representation by us or any other person that the objectives and plans set forth in this Annual Report will be achieved.

In this Annual Report, references to the “Company,” “we,” “us,” “our” or similar terms refer to Generation Income Properties, Inc., a Maryland corporation, together with its consolidated subsidiaries, including Generation Income Properties, L.P., a Delaware limited partnership, which we refer to as our operating partnership (the “Operating Partnership”). As used in this Annual Report, an affiliate, or person affiliated with a specified person, is a person that directly or indirectly, through one or more intermediaries, controls or is controlled by, or is under common control with, the person specified.

Item 1. Business

We are an internally managed real estate investment company focused on acquiring and managing income-producing retail, office and industrial properties net leased to high quality tenants in major markets throughout the United States. With interest rates at historical lows, we believe our focus on owning properties leased to investment grade or creditworthy tenants provide attractive risk adjusted returns through current yields, long term appreciation and tenant renewals. As of December 31, 2020, 78.6% of our base rent was received from tenants that have an investment grade credit rating of “BBB-” or higher and 100% of our rent was paid in full.

We believe that single-tenant commercial properties, as compared with shopping centers, malls, and other traditional multi-tenant properties, offer a distinct investment advantage since single-tenant properties generally require less management and operating capital and have less recurring tenant turnover than do multi-tenant properties.

Given the stability and predictability of the cash flows, many net leased properties are held in family trusts, providing us an opportunity to acquire these properties for tax deferred units while giving the owners potential liquidity through the conversion of the units for freely tradable shares of stock.

- 1 -

We intend to continue to operate our existing portfolio of commercial real estate properties and acquire additional freestanding, single-tenant commercial properties. Once we qualify for taxation as a REIT, we intend to make regular cash distributions to our stockholders out of our cash available for distribution, typically on a quarterly basis. Generally, our policy will be to pay distributions from cash flow from operations. However, our distributions may be paid from sources other than cash flows from operations, such as from the proceeds of offerings, borrowings or distributions in kind.

We were incorporated in Maryland on June 19, 2015. Our business and registered office is located at 401 East Jackson Street, Suite 3300, Tampa, Florida 33602. We intend to operate in conformity with the requirements for qualification and taxation as a REIT under U.S. federal income tax laws. We have not qualified as a REIT to date and will not be able to satisfy the requirements of operating as a REIT until after we expand our shareholder base.

We and our Operating Partnership were organized to operate using an UPREIT structure. We use an UPREIT structure because a sale of property directly to another person or entity generally is a taxable transaction to the selling property owner. In an UPREIT structure, a seller of a property that desires to defer taxable gain on the sale of its property may transfer the property to the Operating Partnership in exchange for common units in the Operating Partnership and defer taxation of gain until the seller later disposes of its common units in the Operating Partnership. Using an UPREIT structure may give us an advantage in acquiring desired properties from persons who may not otherwise sell their properties because of unfavorable tax results.

As of December 31, 2020, we owned 60.7% of the outstanding common units in the Operating Partnership and outside investors own 39.3%.

Business Objectives and Investment Strategy

We intend to acquire and manage a diversified portfolio of high quality net leased properties that generates predictable cash flows and capital appreciation over market cycles. We expect that these properties generally will be net leased to a single-tenant. Under a net lease, the tenant typically bears the responsibility for most or all property related expenses such as real estate taxes, insurance, and maintenance costs. We believe this lease structure provides us with stable cash flows over the term of the lease, and minimizes the ongoing capital expenditures. We seek to identify properties in submarkets with high barriers to entry for development and where valuation is frequently influenced by local real estate market conditions and tenant needs.

Focus on Real Estate Fundamentals: We have observed that the market for properties with bond type net leased structures, lease terms greater than ten years, and limited rent escalators upon renewal are exposed to many of the same operational and market risks as other net leased properties while providing lower returns due to competition. We believe that focusing on traditional real estate fundamentals allows us to target properties with shorter lease terms, modified net leases or vacancy and thereby may allow us to generate superior returns.

Target Markets with Attractive Characteristics: We plan to concentrate our investment activity in select target markets with the following characteristics: high quality infrastructure, diversified local economies with multiple economic drivers, strong demographics, pro-business local governments and high quality local labor pools. We believe that these markets offer a higher probability of producing long term rent growth and capital appreciation.

Target Strategic Net Leased Properties: We target properties that offer unique strategic advantages to a tenant or an industry and can therefore be acquired at attractive yields relative to the underlying risk. We look for properties that are difficult or costly to replicate due to a specific location, special zoning, unique physical attributes, below market rents or a significant tenant investment in the facility, all of which contribute to a higher probability of tenant renewals. Examples of specialized properties include our Pratt & Whitney manufacturing facility located in Huntsville, Alabama whose specialized equipment is unique to such a facility and the GSA (US Navy) occupied building in Norfolk, Virginia due to the tenant’s buildout for IT and security. We target properties if we believe they are critical to the ongoing operations of the tenant and the profitability of its business. We believe that the profitability of the operations and the difficulty in replicating or moving operations reflect the importance of the property to the tenant’s business.

Target Investments that Maximize Growth Potential: We focus on net leased investment properties where, in our view, there is the potential to invest incremental capital to accommodate a tenant’s business, extend lease terms and increase the value of a property. We believe these opportunities can generate attractive returns due to the nature of our relationship with the tenant.

- 2 -

Disciplined Underwriting & Risk Management

We actively manage and regularly review each of our properties for changes in the underlying business, credit of the tenant and market conditions. Before acquiring a property, we review the terms of the management contract to ensure our team is able to maximize cash flow capital appreciation through potential lease renewals and/or potential re-tenanting. Additionally, we monitor any required capital improvements that would lead to increased rental income or capital appreciation over time. We focus on active management with the tenants upon the acquisition of an asset since our experience in the single-tenant, commercial real estate industry indicates that active management and fostering tenant relationships has the potential to positively impact long-term financial outcomes, such as:

• | better communication with corporate level and unit level staff to determine ongoing company and location-specific performance, strategic goals and directives; |

|

|

• | the ability to hold a tenant accountable for property maintenance during occupancy in order to reduce the probability of future deferred maintenance expenses; and |

|

|

• | the ability to develop relationships with tenants as an active participant in their occupancy which can lead to better communication during times of potential negotiations. |

Underwriting Process

Our extensive underwriting process evaluates key fundamental value drivers that we believe will attract long-term tenants and result in property appreciation over time. This comprehensive pre-ownership analysis led by our CEO (David Sobleman, who has over 15 years in different capacities within the net lease commercial real estate) helps us to assess location level performance, including the possible longevity of tenant occupancy throughout the primary lease term and option periods.

We assess target markets and properties using an extensive underwriting and evaluation process, including:

• | offering materials review; |

|

|

• | property and tenant lease information; |

|

|

• | in depth conversations with offering agent, local brokers and property management companies; |

|

|

• | thorough credit underwriting of the tenant; |

|

|

• | review of tenant’s historical performance in the specific market and their nationwide trend to determine potential longevity of the asset and tenant’s business model; |

|

|

• | market real estate dynamics, including macroeconomic market data and market rents for potential rental rate changes after initial lease term; |

|

|

• | evaluation of business trends for local real estate demand specifics and competing business locations; |

|

|

• | review of asset level financial performance; |

|

|

• | pre-acquisition discussions with asset manager to confirm property specific reserve amounts and potential future capital expenditures; |

|

|

• | review of property’s physical condition and related systems; and |

|

|

• | financial modeling to determine our preliminary baseline pricing. |

Specific acquisition criteria may include, but is not limited to, the following:

• | properties with existing, long-term leases of approximately seven years or greater; |

|

|

• | premier locations and facilities with multiple alternative uses; |

- 3 -

• | sustainable rents specific to a tenants’ location that may be at or below market rents; |

|

|

• | investment grade or strong credit tenant; |

|

|

• | properties not subject to long-term management contracts with management companies; |

|

|

• | opportunities to expand the tenants’ building and/or implement value-added operational improvements; and |

|

|

• | population density and strong demand growth characteristics supported by favorable demographic indicators. |

Competitive Strengths

We expect the following factors will benefit our company as we implement our business strategy:

• | Focused Property Investment Strategy. We have invested and intend to invest primarily in assets that are geographically located in prime markets throughout the United States, with an emphasis on the major primary and coastal markets, where we believe there are greater barriers to entry for the development of new net lease properties. |

|

|

• | Experienced Board of Directors. We believe that we have a seasoned and experienced board of directors that will help us achieve our investment objectives. In combination, our directors have approximately 110 years of experience in the real estate industry. |

|

|

• | Real Estate Industry Leadership and Networking. We are led by our Chairman and President, David Sobelman. He founded the company after serving in different capacities within the net lease commercial real estate market. Mr. Sobelman has held various roles within the single-tenant, net lease commercial real estate investment market over the past 15 years, including investor, asset manager, broker, owner, analyst and advisor. Mr. Sobelman started his real estate career in 2005 as a real estate analyst and ultimately emerged into a Managing Partner of a solely-focused, triple net lease commercial real estate firm. He has procured or overseen numerous transactions that ranged from small, private investments to portfolio transactions with individual aggregate values of approximately $69 million. Additionally, Mr. Sobelman considers himself a pioneer in implementing hands-on management of net leased properties in order to potentially maintain or increase the value of any one asset. He has overseen or actively participated in single-tenant real estate management since 2010. |

|

|

• | Established and Developing Relationships with Real Estate Financing Sources. We believe our existing relationships with institutional sources of debt financing could provide us with attractive and competitive debt financing options as we grow our property portfolio, and provide us the opportunity to refinance our existing indebtedness. |

|

|

• | Existing Acquisition Pipeline. We believe our extensive network of long standing relationships will provide us with access to a pipeline of acquisition opportunities that will enable us to identify and capitalize on what we believe are attractive acquisition opportunities for our leasing efforts. |

|

|

• | Growth-Oriented, Flexible and Conservative Capital Structure. We believe our capital structure will provide us with an advantage over many of our private and public competitors. |

|

|

• | Capital Structure Flexibility. We believe having a flexible capital structure provides us with the ability to quickly acquire properties that are priced advantageous to us while allowing us to manage our debt requirements and generate appropriate risk-adjusted returns. As of March 5, 2021, we had signed a term sheet with a financial institution for up to $50 million of borrowings. We expect to finalize this term sheet into a signed agreement over the next 90 days, but we can provide no assurance that we will enter into an agreement for this borrowing within this timeframe or at all. |

Financing Strategies

Our long-term goal is to maintain a lower-leveraged capital structure and lower outstanding principal amount of our consolidated indebtedness. Individual assets may be more highly leveraged. Over time, we intend to reduce our debt positions through financing our long-term growth with equity issuances and some debt financing having staggered maturities. Our debt may include mortgage debt secured by our properties and unsecured debt. Over a long-term period, we intend to maintain lower levels of debt encumbering the company, its assets and/or the portfolio.

- 4 -

Our Current Portfolio

The following are characteristics of our seven properties as of December 31, 2020:

• | Creditworthy Tenants. Approximately 78% of our portfolio’s annualized base rent as of December 31, 2020 was derived from tenants that have (or whose parent company has) an investment grade credit rating from a recognized credit rating agency of “BBB-” or better. |

|

|

• | 100% Occupied with Long Duration Leases. Our portfolio is 100% leased and occupied. The leases in our initial portfolio have a weighted average remaining lease term of approximately 7.0 years (based on annualized base rent as of December 31, 2020). |

|

|

• | Contractual Rent Growth. Approximately 44% of the leases in our portfolio (based on annualized base rent as of December 31, 2020) provide for increases in contractual base rent during futures years of the current term. In addition, approximately 65% (based on annualized base rent as of December 31, 2020) of the leases in our initial portfolio allow for increases in base rent during the lease extension periods. |

|

|

• | Average Effective Annual Rental per Square Foot. Average effective annual rental per square foot is $17.79. |

The table below presents an overview of the seven properties in our portfolio as of December 31, 2020, unless otherwise indicated:

|

|

|

|

| Tenant |

| |||||

| S&P |

|

|

| Extension |

| |||||

|

| Rentable |

| Credit | Lease | Remaining | Options | Contractual | Annualized | Annualized | Base Rent |

Property | Property | Square |

| Rating | Expiration | Term | (Number | Rent | Base Rent | Base Rent | as a % of |

Type | Location | Feet | Tenant(s) | (1) | Date | (Years) | x Years) | Escalations | (2) | Sq. Ft. | Total |

Retail | Washington, DC | 3,000 | 7-Eleven Corporation | AA- | 3/31/2026 | 5.3 | 2 x 5 | Yes | $ 126,853 | $ 42.28 | 3.8% |

Retail | Tampa, FL | 2,200 | Starbucks | BBB+ | 2/29/2028 | 7.3 | 4 x 5 | Yes | $ 182,500 | $ 82.95 | 5.4% |

Industrial | Huntsville,AL | 59,091 | Pratt & Whitney Automation, Inc. | BBB+ | 1/31/2029 | 8.2 | 2 x 5 | Yes | $ 684,996 | $ 11.59 | 20.3% |

Retail | Cocoa, FL | 15,120 | Walgreen Co. (3) | BBB | 12/31/2029 | 9.1 | 3 x 5 | No | $ 313,480 | $ 20.73 | 9.3% |

Office | Norfolk, VA | 49,902 | General Services Administration of the United State of America | AA+ | 9/17/2028 | 7.8 | — | No | $ 882,476 | $ 17.68 | 26.1% |

| Norfolk,VA | 22,247 | Maersk Line, Limited | BBB- | 12/1/2021 | 0.9 | 2 x 5 | Yes | $ 343,377 | $ 15.43 | 10.2% |

Office | Norfolk,VA | 34,847 | PRA Holdings, Inc. (4) | BB+ | 8/31/2027 | 6.8 | 1 x 5 | Yes | $ 724,820 | $ 20.80 | 21.4% |

Retail | Tampa, FL | 3,500 | Sherwin Williams | BBB | 7/31/2028 | 7.7 | 5 x 5 | Yes | $ 120,750 | $ 34.50 | 3.5% |

|

|

|

|

|

|

|

|

|

|

|

|

Total |

| 189,907 |

|

|

|

|

|

| $ 3,379,252 |

|

|

__________

(1) | Tenant, or tenant parent, rated entity. |

|

|

(2) | Annualized cash base rental income in place as of December 31, 2020. Our leases do not include tenant concessions or abatements. |

|

|

(3) | Tenant has the right to terminate on the following dates: July 31, 2028, July 31, 2033, July 31, 2038, July 31, 2043, July 31, 2048, July 31, 2053, July 31, 2058 and July 31, 2063. |

|

|

(4) | Tenant has the right to terminate the lease on August 31, 2024 subject to certain conditions. |

As of December 31, 2020, we owned seven assets described in more detail below:

• | On June 29, 2017, we acquired through our wholly-owned Delaware subsidiary, GIPDC 3707 14th ST, LLC, a 3,000 square foot single-tenant retail condo located at 3707-3711 14th Street, NW in Washington, D.C. (the “D.C. Property”) for approximately $2.6 million in total consideration, with 7-Eleven Corporation as a continuing tenant. The lease for the D.C. Property is a triple-net lease with an initial term of ten years, ending March 31, 2026, with two options to extend the term of the lease for two additional five-year periods. The base rent is $9,833.33 per month for the first five years of the lease, increasing to $10,817.00 per month for years six through ten of the lease term. We have granted a first priority mortgage on |

- 5 -

| the D.C. property and each of the Tampa, Florida and Huntsville, Alabama properties described below, to secure a $11.3 million loan from DBR Investments Co. Limited to GIPDC 3707 14TH ST, LLLC and two of our other wholly-owned subsidiaries, GIPFL 1300 S DALE MABRY, LLC and GIPAL JV 15091 SW ALABAMA 20, LLC (the “DC/Tampa/Alabama Loan”). The DC/Tampa/Alabama Loan matures in February 2030 and the loan agreement for this loan contains standard affirmative and negative covenants, including prohibitions on additional liens on the collateral, financial reporting obligations and maintenance of insurance, as well as a covenant that the properties, securing the loan, maintain a debt service coverage ratio of not less than 1.25:1.00, measured quarterly. Mr. Sobelman has personally guaranteed certain recourse obligations and liabilities with respect to the DC/Tampa/Alabama Loan. |

|

|

• | On April 4, 2018, we acquired through our wholly-owned Delaware subsidiary, GIPFL 1300 S. DALE MABRY, LLC, a 2,200 square foot single-tenant retail stand-alone property located at 1300 South Dale Mabry Highway in Tampa, Florida (the “Tampa Property”) for approximately $3.6 million in total consideration, with a corporate Starbucks Coffee as a continuing tenant. The lease for the Tampa Property is a triple-net lease with an initial term of ten years, ending February 29, 2028, with two options to extend the term of the lease for four additional five-year periods. The base rent for years one through five of the lease term is $15,208.33 per month, increasing to $16,729.17 per month for years six through ten of the lease term. The lease includes a right of first offer in favor of Starbucks in the event we decide to sell the Tampa Property to a third party purchaser. As described above, we have granted a first lien mortgage on the Tampa Property to secure the DC/Tampa/Alabama Loan and Mr. Sobleman has personally guaranteed certain recourse obligations and liabilities with respect to the loan. Starbucks Corporation files annual reports on Form 10-K and quarterly reports on Form 10-Q with the SEC. |

|

|

• | On December 20, 2018, we acquired a 59,000 square foot single-tenant industrial building located at 15091 Alabama Highway 20, in Huntsville, AL (the “Alabama Property”) for approximately $8.4 million in total consideration, with Pratt & Whitney Automation, Inc. as a continuing tenant. The fee owner of the Alabama Property is our subsidiary GIPAL JV 15091 SW ALABAMA 20, LLC (the “Alabama Subsidiary”). The acquisition was funded in part by a capital contribution of approximately $2.2 million to the Alabama Subsidiary by the holder of all of the outstanding Class A Preferred membership units in the Alabama Subsidiary (the “Alabama Preferred Member”). We redeemed 100% of the Alabama Preferred Member’s membership interests in the Alabama Subsidiary on December 18, 2019 for approximately $2.4 million in cash, using existing cash and the proceeds from a $1.9 million secured non-convertible promissory note issued by the Operating Partnership to the Clearlake Preferred Member which is secured by all of the personal and fixture property assets of the Operating Partnership. This note accrues interest at a 10% per annum rate, which is payable monthly to the Clearlake Preferred Member. The principal amount of the note will become due and payable on December 16, 2021. On February 12, 2020 we prepaid a portion of the outstanding principal of the $1.9 million note issued to the Clearlake Preferred Member. The remaining portion of the acquisition of the Alabama Property was funded with a $6.1 million mortgage loan, that was refinanced in February 2020 using the proceeds of the DC/Tampa/Alabama Loan. As described above, we have granted a first lien mortgage on the Alabama Property to secure the DC/Tampa/Alabama Loan and Mr. Sobleman has personally guaranteed certain recourse obligations and other liabilities with respect to the loan. The lease for the Alabama Property is a triple-net lease with an initial term of ten years, ending January 31, 2029, provided Pratt & Whitney has the option to terminate the lease effective January 31, 2024 upon not less than six months’ prior written notice. If Pratt & Whitney elects to terminate the lease on January 31, 2024, it is required to pay us a termination payment of $493,612.70, to reimburse us for the unamortized portions of the tenant improvements and real estate leasing fees previously paid by us, and a termination fee. The monthly rent under the lease is $57,083 per month. United Technologies Corporation, the parent company of Pratt and Whitney Corporation, files annual reports on Form 10-K and quarterly reports on Form 10-Q with the SEC. |

|

|

• | On September 11, 2019, we acquired an approximately 15,000-square-foot, single-tenant building located at 1106 Clearlake Road, Cocoa, Florida (the “Cocoa Property”) for total consideration of approximately $4.5 million, with Walgreen Co. as a continuing tenant (“Walgreens”). The acquisition was funded in part with debt financing of approximately $3.4 million and in part with a capital contribution of $1.2 million to our Delaware operating subsidiary, GIPFL JV 1106 Clearlake Road, LLC (the “Clearlake Subsidiary”), by the holder of all of the outstanding Class A Preferred membership units in the Clearlake Subsidiary (the “Clearlake Preferred Member”). The Clearlake Preferred Member will be paid a 10% annual preferred return on its capital contribution. The Clearlake Preferred Member’s interest in the Clearlake Subsidiary is a “Redeemable Non-Controlling Interest” because it is a non-controlling interest and is redeemable for cash or common units in the Operating Partnership at the election of the Clearlake Preferred Member after 24 months. The $3.4 million loan incurred in connection with the acquisition of the Cocoa Property is secured by a first priority mortgage on the Cocoa Property in favor of American Momentum Bank (the “Cocoa American Momentum Loan”). The loan agreement for Cocoa American Momentum Loan contains standard affirmative and negative covenants, including prohibitions on additional liens on the collateral, financial reporting obligations and maintenance of insurance, as well as a covenant that we maintain a minimum DSCR of not less than 1.1 to 1.0, measured annually. The loan agreement for the Cocoa American Momentum Loan also provides for a |

- 6 -

| mandatory repayment in full twelve months from the date Walgreens formally notifies us that it will cease operations at the Cocoa Property. The Cocoa American Momentum Loan matures September 11, 2021, and Mr. Sobelman has personally guaranteed the repayment of up to fifty percent of the outstanding principal due under the Cocoa American Momentum Loan. The Walgreens lease term expires on July 31, 2068, provided Walgreens has the option to terminate the lease effective July 31, 2028, July 31, 2033, July 31, 2038, July 31, 2043, July 31, 2048, July 31, 2053, July 31, 2058 and July 31, 2063 upon at least six months prior written notice. The rent is fixed during the lease term and is equal to $26,123.35 per month. The lease includes a right of first refusal in favor of Walgreens in the event we receive a bona fide offer to purchase the Cocoa Property during the term of the lease. Walgreens Boots Alliance, Inc. files annual reports on Form 10-K and quarterly reports on Form 10-Q with the SEC. |

|

|

• | On September 30, 2019 we acquired through our wholly-owned Delaware subsidiary, GIPVA 2510 Walmer Ave, LLC, an approximately 72,000 square foot two-tenant office building located at 2510 Walmer Avenue, Norfolk, Virginia (the “Walmer Property”) for total consideration of approximately $11.5 million, with each of the General Services Administration of the United States of America and Maersk Line, Limited (“Maersk”) as continuing tenants. The acquisition of the Walmer Property was funded by issuing 248,250 common units in the Operating Partnership, priced at $20.00 per unit, for a total value of $4,965,000, plus an additional $822,000 in cash, and the assumption of approximately $6.0 million of existing mortgage debt. The debt assumed in connection with the acquisition has been refinanced by a new loan from Bayport Credit Union in the amount of approximately $8.3 million (the “Walmer Avenue Bayport Loan”), and the refinancing resulted in approximately $1,206,000 of cash. The Walmer Avenue Bayport Loan matures on September 30, 2024 and Mr. Sobelman has provided a guaranty of the Borrower’s nonrecourse carve out liabilities and obligations in favor of Bayport Credit Union. The loan agreement for the Walmer Avenue Bayport Loan contains standard affirmative and negative covenants, including prohibitions on additional liens on the collateral, financial reporting obligations and maintenance of insurance, as well as a covenant that we maintain a minimum DSCR with respect to the Walmer Avenue Property of not less than 1.25 to 1.0, measured annually on a trailing twelve month basis. In addition, the loan agreement requires that we also maintain a minimum DSCR of not less than 1.25 to 1.0 with respect to our Corporate Boulevard Property described below, and a minimum DSCR across our entire portfolio of properties of not less than 1.0 to 1.0, in each case measured annually on a trailing twelve month basis. The lease with the United States of America at the Walmer Property (the “GSA Lease”) has a term ending September 17, 2028 following the exercise of an option to extend the term of the lease for one five-year period. The annual rent payable under the GSA Lease is $882,476.30, payable monthly in arrears at the rate of $73,539.69 per month, subject to annual adjustment for increases and decreases in real estate taxes and operating costs associated with the Walmer Property. The lease with Maersk at the Walmer Property (the “Maersk Lease”) has an initial term of five years, commencing December 19, 2016 and ending December 1, 2021, with two options to extend the term of the lease for two additional five-year periods upon not less than six months written notice. The current base rent of the Maersk Lease is $29,052.30 per month, with the base rent increasing 3% on each anniversary of the commencement date during the term. The Maersk Lease includes a right of first refusal in favor of Maersk to lease space in the Walmer Property that is contiguous to the Maersk leased space as such space becomes available to third parties. The Maersk Lease also contains an expansion option in favor of Maersk to expand their leased premises into any available contiguous space at the Walmer Property. |

|

|

• | On September 30, 2019 we acquired through our wholly-owned Delaware subsidiary, GIPVA 130 Corporate Blvd, LLC, an approximately 35,000 square foot single-tenant office building located at 130 Corporate Boulevard, Norfolk, Virginia (the “Corporate Boulevard Property”), for total consideration of approximately $7.1 million, with PRA Holdings, Inc. as a continuing tenant. The acquisition was funded with the issuance of 101,663 common units in the Operating Partnership, priced at $20.00 per unit, for a total value of $2,033,250 plus an additional $100,000 in cash, and the assumption of approximately $5.2 million of mortgage debt with Bayport Credit Union (the “Corporate Boulevard Bayport Loan”). The Corporate Boulevard Bayport Loan matures on October 23, 2024 and Mr. Sobelman has provided a guaranty of the Borrower’s nonrecourse carve out liabilities and obligations in favor of Bayport Credit Union. The loan agreement for the Corporate Boulevard Bayport Loan contains standard affirmative and negative covenants, including prohibitions on additional liens on the collateral, financial reporting obligations and maintenance of insurance, as well as a covenant that we maintain a minimum DSCR with respect to the Corporate Boulevard Property of not less than 1.25 to 1.0, measured annually on a trailing twelve month basis. In addition, the loan agreement requires that we also maintain a minimum DSCR of not less than 1.25 to 1.0 with respect to our Walmer Avenue Property, and a minimum DSCR across our entire portfolio of properties of not less than 1.0 to 1.0, in each case measured annually on a trailing twelve month basis. The lease with PRA Holdings expires on August 31, 2027, with one option to extend the term of the lease for one additional five year period. PRA Holdings has a one-time option to terminate the lease effective August 31, 2024 upon not less than 12 months prior notice and payment of a $236,372.77 termination fee. The current monthly rent is $59,212.99, increasing 3% per annum each September if the Consumer Price Index is greater than 3% in any year, or increasing annually at 1.5% per annum if the Consumer Price Index is less than 3% in any year. The lease includes a right of first refusal in favor of PRA Holdings to lease contiguous vacant available space in the Corporate Boulevard Property. |

- 7 -

• | On November 30, 2020 we acquired through our wholly-owned Delaware subsidiary, GIPFL 508 S Howard Ave, LLC, an approximately 3,500 square foot single-tenant retail building located at 508 S Howard Ave, Tampa, Florida (the “Sherwin Williams Property”), for total consideration of approximately $1.8 million, with Sherwin-Williams, Inc. as a continuing tenant. The acquisition was funded with the issuance of 24,309 common units in the Operating Partnership, priced at $20.00 per unit, for a total value of $486,180 plus an additional $1,000 in cash, and the assumption of approximately $1.3 million of mortgage debt with Valley Bank (the “Sherwin-Williams Loan”). The Sherwin-Williams Loan matures on August 10, 2028 and Mr. Sobelman has provided a guaranty of the Borrower’s recourse carve out liabilities and obligations in favor of Valley Bank. The loan agreement for the Sherwin-Williams Loan contains standard affirmative and negative covenants, including prohibitions on additional liens on the collateral, financial reporting obligations and maintenance of insurance, as well as a covenant that we maintain a minimum DSCR with respect to the Sherwin-Williams Property of not less than 1.20 to 1.0, measured annually on a trailing twelve month basis. The lease with Sherwin-Williams expires on July 31, 2028, with five options to extend the term of the lease for one additional five year period with 10% increase in the base rent upon each extension. The current monthly rent is $10,062. The lease includes a right of first refusal in favor of Sherwin-Williams in the event we receive a bona fide offer to purchase the Cocoa Property during the term of the lease. Sherwin-Williams, Inc. files annual reports on Form 10-K and quarterly reports on Form 10-Q with the SEC. |

Subsequent to December 31, 2020, we acquired the following:

• | On August 24, 2018, we entered into a Purchase and Sale Agreement with Maritime Woods Development, LLC for the purchase of an approximately 5,800-square-foot free-standing condominium unit located at 7100 Maritime Woods Drive, Manteo, North Carolina, solely occupied by the United States of America, for a total consideration of approximately $1.7 million. The single-tenant property is in a coastal area of North Carolina. During our due diligence with respect to the North Carolina Property, we discovered certain deficiencies with respect to the condominium documents relating to the North Carolina Property and the parties entered into an amendment to the Purchase and Sale Agreement on November 21, 2018 extending our inspection period with respect to the North Carolina Property to within forty-five days of our acceptance and satisfaction of the corrective actions taken by the seller with respect to the deficiencies. We completed the acquisition of the condominium unit on February 4, 2021 with approximately $1.3 million of debt and approximately $500,000 of preferred equity provided from a Joint Venture Partner. |

COVID-19 Update

To date our business has not been significantly impacted by the COVID-19 pandemic. While several of our national tenants have publicly reported financial challenges they have suffered because of the COVID-19 pandemic, none of our tenants have requested rent abatements or reductions from us. One of our national tenants informed all of its landlords in May about the financial challenges it was suffering and referenced concessions to lease terms and base rent it would request. However, to date that tenant has not requested any concessions from us. While obtaining financing during the COVID-19 pandemic has been challenging, we are beginning to see more lenders enter into new financings for projects like ours. The impact of the COVID-19 pandemic on our business is still uncertain and will be largely dependent on future developments. Please see “Risk Factors” herein for further information.

Potential Acquisition Pipeline

We have a network of long-standing relationships with real estate developers, individual and institutional real estate owners, national and regional lenders, brokers, tenants and other market participants. We believe this network will provide us with market intelligence and access to a potential pipeline of attractive acquisition opportunities.

We are continually engaging in internal research as well as informal discussions with various parties regarding our potential interest in these types of potential acquisitions. As of December 31, 2020, we have not specifically targeted, and are not a party to any agreement to purchase. There is no assurance that any currently available properties will remain available, or that that we will pursue or complete any of these potential acquisitions, at prices acceptable to us or at all.

- 8 -

Property and Asset Management Agreements

We had previously engaged 3 Properties, a business managed by our President, to provide asset management services for our properties. These agreements were terminated effective August 31, 2020. We now manage these properties in-house. Except for the two properties in Norfolk described below, we now manage our properties in-house.

We have engaged Colliers International Asset Services to provide property management services to our two properties in Norfolk, Virginia. The agreements provide for us to pay Colliers International Asset Services a management fee equal to 2.5% of the gross collected rent of each of the two properties (inclusive of tenant expense reimbursements) as well as a construction supervision fee for any approved construction. The agreements are for a term of one year and automatically renew on a month-to-month basis thereafter.

Future Rental Payment

The following table presents future minimum base rental cash payments due to the Company over the next five calendar years and thereafter as of December 31, 2020:

| Future |

| |

2021 | $ | 3,379,000 |

|

2022 |

| 3,049,000 |

|

2023 |

| 3,067,000 |

|

2024 |

| 3,064,000 |

|

2025 |

| 3,076,000 |

|

Thereafter |

| 7,823,000 |

|

| $ | 23,458,000 |

|

__________

(1) | Rental income estimates adjusted to contemplate rent increases. A lease that has a term of 50 years is assumed to terminate after 10 years. |

Employees

As of March 1, 2021, we had one part-time employee and three full time employees, including David Sobelman, who serves our Chief Executive Officer, President and Secretary, and Richard Russell who serves as our Chief Financial Officer and Treasurer on a part-time basis. We plan to use consultants, attorneys, and accountants, as necessary.

Operation through Our Operating Partnership

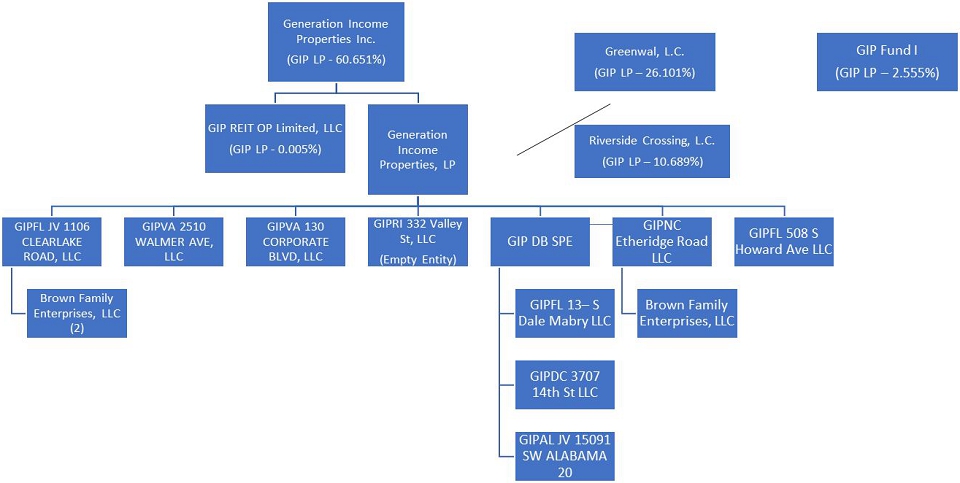

We are the sole general partner of Generation Income Properties, L.P., our Operating Partnership, which is the subsidiary through which we conduct substantially all of our operations. Through its own subsidiaries, the Operating Partnership owns all of our properties, as shown below. We are the sole general partner of Generation Income Properties, L.P., which is the subsidiary through which we conduct substantially all of our operations. As of March 1, 2021, we own 60.7% of the outstanding common units in the Operating Partnership and outside investors own 39.3%. The following chart shows the structure of our company as of December 31, 2020:

- 9 -

__________

(1) | Brown Family Enterprises, LLC, the Clearlake Preferred Member, owns a redeemable limited partnership interest in GIPFL JV 1106 Clearlake Road, LLC. |

Market Opportunity

According to Real Capital Analytics and Colliers International U.S. Research Report “Single Tenant Net Lease Retail H2 2018” report, the dollar volume of single-tenant net lease (STNL) retail property transactions fell 10.6% in 2018 versus 2017, while the number of transactions declined 2.6% year over year. After peaking in 2015, the transaction volume has declined to below 2013 levels indicating additional opportunities will begin to arise in coming years. This decrease followed a dramatic increase in transaction volume from 2009 through 2014, during which period attractive financing was widely available and industry fundamentals were generally favorable.

We believe that a number of factors, including debt defaults, maturity defaults and lack of available financing and under-capitalized owners will increase pressure on certain net lease owners to sell properties at prices that we believe are attractive and that transaction volumes will continue to decrease over the next several years.

Our Opportunity

We intend to continue to raise money through securities offerings to continue to grow. We currently own eight properties which were acquired with debt, joint venture equity and using proceeds from a prior offering. We intend to acquire additional properties when we raise sufficient funds and identify suitable properties.

Competition

The net lease industry is highly competitive. We compete to acquire properties with other investors, including traded and non-traded public REITs, private equity investors and institutional investment funds, many of which have greater financial resources than we do, a greater ability to borrow funds to acquire properties and the ability to accept more risk than we can prudently manage. This competition increases the demand for the types of properties in which we wish to invest and, therefore, reduces the number of suitable acquisition opportunities available to us and increases the prices paid for such acquisition. This competition will increase if investments in real estate become more attractive relative to other forms of investment.

- 10 -

As a landlord, we will compete for tenants in the multi-billion dollar commercial real estate market with numerous developers and owners of properties, many of which own properties similar to ours in the same markets in which our properties are located. Many of our competitors will have greater economies of scale, have access to more resources and have greater name recognition than we do. If our competitors offer space at rental rates below current market rates or below the rental rates we charge our tenants, we may lose our tenants or prospective tenants and we may be pressured to reduce our rental rates or to offer substantial rent abatements, tenant improvement allowances, early termination rights or below-market renewal options in order to retain tenants when our leases expire.

Environmental Matters

To control costs, we intend to limit our investments to properties that are environmentally compliant or that do not require extensive remediation upon acquisition. To do this, we intend to conduct assessments of properties before we decide to acquire them. These assessments, however, may not reveal all environmental hazards. In certain instances we will rely upon the experience of our management and we expect that in most cases we will request, but will not always obtain, a representation from the seller that, to its knowledge, the property is not contaminated with hazardous materials.

Additionally, we seek to ensure that many of our leases will contain clauses that require a tenant to reimburse and indemnify us for any environmental contamination occurring at the property. We do not intend to purchase any properties that have known environmental deficiencies that cannot be remediated.

Federal, state and local environmental laws and regulations regulate, and impose liability for, releases of hazardous or toxic substances into the environment. Under various of these laws and regulations, a current or previous owner, operator or tenant of real estate may be required to investigate and clean up hazardous or toxic substances, hazardous wastes or petroleum product releases or threats of releases at the property, and may be held liable to a government entity or to third parties for property damage and for investigation, cleanup and monitoring costs incurred by those parties in connection with the actual or threatened contamination. These laws typically impose cleanup responsibility and liability without regard to fault, or whether or not the owner, operator or tenant knew of or caused the presence of the contamination. The liability under these laws may be joint and several for the full amount of the investigation, cleanup and monitoring costs incurred or to be incurred or actions to be undertaken, although a party held jointly and severally liable may seek to obtain contributions from other identified, solvent, responsible parties of their fair share toward these costs. In addition, under the environmental laws, courts and government agencies have the authority to require that a person or company who sent waste to a waste disposal facility, such as a landfill or an incinerator, must pay for the cleanup of that facility if it becomes contaminated and threatens human health or the environment. Any of these cleanup costs may be substantial, and can exceed the value of the property. The presence of contamination, or the failure to properly remediate contamination, on a property may adversely affect the ability of the owner, operator or tenant to sell or rent that property or to borrow using the property as collateral, and may adversely impact our investment in that property.

Furthermore, various court decisions have established that third parties may recover damages for injury caused by property contamination. For instance, a person exposed to asbestos while occupying a net lease may seek to recover damages if he or she suffers injury from the asbestos. Lastly, some of these environmental laws restrict the use of a property or place conditions on various activities. An example would be laws that require a business using chemicals (such as swimming pool chemicals at a net lease property) to manage them carefully and to notify local officials that the chemicals are being used.

We could be responsible for any of the costs discussed above. The costs to clean up a contaminated property, to defend against a claim, or to comply with environmental laws could be material and could adversely affect the funds available for distribution to our shareholders. Prior to any acquisition of property, we will seek to obtain environmental site assessments to identify any environmental concerns at the property. However, these environmental site assessments may not reveal all environmental costs that might have a harmed our business, assets, results of operations or liquidity and may not identify all potential environmental liabilities.

As a result, we may become subject to material environmental liabilities of which we are unaware. We can make no assurances that (1) future laws or regulations will not impose material environmental liabilities on us, or (2) the environmental condition of our net lease properties will not be affected by the condition of the properties in the vicinity of our net lease properties (such as the presence of leaking underground storage tanks) or by third parties unrelated to us.

Insurance

We require our tenants to maintain liability and property insurance coverage for the properties they lease from us pursuant to net leases. Pursuant to the leases, our tenants may be required to name us (and any of our lenders that have a mortgage on the property leased by the tenant) as additional insureds on their liability policies and additional named insured and/or loss payee (or mortgagee, in the case of our lenders) on their property policies. All tenants are required to maintain casualty coverage. Depending on the location of

- 11 -

the property, losses of a catastrophic nature, such as those caused by earthquakes and floods, may be covered by insurance policies that are held by our tenants with limitations such as large deductibles or co-payments that a tenant may not be able to meet. In addition, losses of a catastrophic nature, such as those caused by wind/hail, hurricanes, terrorism or acts of war, may be uninsurable or not economically insurable. In the event there is damage to any of our properties that is not covered by insurance and such properties are subject to recourse indebtedness, we will continue to be liable for any indebtedness, even if these properties are irreparably damaged. In addition to being a named insured on our tenants’ liability policies, we intend to separately maintain commercial general liability coverage with an aggregate limit of $2,000,000. We also intend to maintain full property coverage on all untenanted properties and any other property coverage required by any of our lenders that is not required to be carried by our tenants under our leases.

Jumpstart our Business Startups Act

In April 2012, the Jumpstart Our Business Startups Act (“JOBS Act”) was enacted into law. The JOBS Act provides, among other things, exemptions for emerging growth companies from certain financial disclosure and governance requirements for up to five years.

In general, under the JOBS Act a company is an emerging growth company if its initial public offering (“IPO”) of common equity securities was effected after December 8, 2011 and the company had less than $1.07 billion of total annual gross revenues during its last completed fiscal year. We currently qualify as an emerging growth company, but will no longer qualify after the earliest of:

• | the last day of the fiscal year during which we have annual total gross revenues of $1.07 billion or more; |

|

|

• | the last day of the fiscal year following the fifth anniversary of the first sale of our common equity securities in an offering registered under the Securities Act; |

|

|

• | the date on which we issue more than $1 billion in non-convertible debt securities during a previous three-year period; or |

|

|

• | the date on which we become a large accelerated filer, which generally is a company with a public float of at least $700 million (Exchange Act Rule 12b-2). |

As an emerging growth company, we are eligible to include audited financial statements required for only two fiscal years and limited executive compensation information.

Pursuant to the relief for emerging growth companies under the JOBS Act, our independent registered public accounting firm is not required to file an attestation report on our internal controls over financial reporting and is exempt from the mandatory auditor rotation rules.

In addition, Section 102(b)(1) of the JOBS Act exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a Securities Act registration statement declared effective or do not have a class of securities registered under the Exchange Act) are required to comply with the new or revised financial accounting standard. The decision by companies to “opt out” of the extended transition period for complying with new or revised accounting standards is irrevocable. We are not electing to opt out of the JOBS Act extended accounting transition period. We intend to take advantage of the extended transition period provided under the JOBS Act for complying with new or revised accounting standards.

To the extent we take advantage of the reduced disclosure requirements afforded by the JOBS Act, investors may be less likely to invest in us or may view our shares as a riskier investment than a similarly situated company that does not take advantage of these provisions.

RISK FACTORS

We face risks and uncertainties that could affect us and our business as well as the real estate industry generally. In addition, new risks may emerge at any time, and we cannot predict such risks or estimate the extent to which they may affect our financial performance. These risks could result in a decrease in the value of our common stock.

The occurrence of any of the following risks could materially and adversely affect our business, prospects, financial condition, results of operations and our ability to make cash distributions to our stockholders, which could cause you to lose all or a significant portion of your investment in our common stock. Some statements in this filing, including statements in the following risk factors, constitute forward-looking statements.

- 12 -

Risks Related to Our Business and Properties

The recent coronavirus outbreak could have an adverse effect on our business.

Concerns are rapidly growing about the global outbreak of a novel strain of coronavirus (COVID-19). The virus has spread rapidly across the globe, including the U.S. The pandemic is having an unprecedented impact on the U.S. economy as federal, state and local governments react to this public health crisis, which has created significant uncertainties. These uncertainties include, but are not limited to, the potential adverse effect of the pandemic on the economy, our tenants, customer sentiment in general and general store traffic. As the pandemic continues to grow, consumer fear about becoming ill with the virus and recommendations and/or mandates from federal, state and local authorities to avoid large gatherings of people or self-quarantine may continue. The extent of the impact of the pandemic on our business and financial results will depend largely on future developments, including the duration of the spread of the outbreak within the U.S., the impact on capital and financial markets and the related impact on consumer confidence and spending, all of which are highly uncertain and cannot be predicted. This situation is changing rapidly, and additional impacts may arise that we are not aware of currently.

We have not generated any profit to date and have incurred losses since inception.

We generated $3.5 million and $1.7 million in rental revenues during the year ended December 31, 2020 and 2019, respectively and we have cumulative net losses of approximately $4.2 million from inception to December 31, 2020. We may never become profitable and you may lose your entire investment. As of December 31, 2020, we had total cash (unrestricted and restricted) of approximately $1.1 million, properties with a cost basis of $40.8 million and outstanding debt of approximately $29.5 million.

We have limited operating history and may not be able to successfully operate our business or generate sufficient operating cash flows to make or sustain distributions to our stockholders.

We were organized in June 2015 for the purpose of acquiring and investing in freestanding, single-tenant commercial properties net leased to investment grade tenants. To date we have acquired eight assets. We commenced operations as soon as we were able to raise sufficient funds to acquire our first suitable property. However, our ability to make or sustain distributions to our stockholders will depend on many factors, including our ability to identify attractive acquisition opportunities that satisfy our investment strategy, our success in consummating acquisitions on favorable terms, the level and volatility of interest rates, readily accessible short-term and long-term financing on favorable terms, and conditions in the financial markets, the real estate market and the economy. We will face competition in acquiring attractive net lease properties. The value of the net lease properties that we acquire may decline substantially after we purchase them. We may not be able to successfully operate our business or implement our operating policies and investment strategy successfully. Furthermore, we may not be able to generate sufficient operating cash flow to pay our operating expenses and make distributions to our stockholders.

As an early stage company, we are subject to the risks of any early stage business enterprise, including risks that we will be unable to attract and retain qualified personnel, create effective operating and financial controls and systems or effectively manage our anticipated growth, any of which could have a harmful effect on our business and our operating results.

We currently own eight leased properties.

We currently own eight properties to lease to tenants. We need to raise funds to acquire additional properties to lease in order to grow and generate additional revenue. Because we only own eight properties, the loss of any one tenant (or financial difficulties experienced by one of our tenants) could have a material adverse impact on our business and operations.

Many of our future properties will likely depend upon a single-tenant for all or a majority of their rental income, and our financial condition and ability to make distributions may be adversely affected by the bankruptcy or insolvency, a downturn in the business, or a lease termination of a single-tenant.

We expect that many of our properties will be occupied by only one tenant or will derive a majority of their rental income from one tenant and, therefore, the success of those properties will be materially dependent on the financial stability of such tenants. Lease payment defaults by tenants could cause us to reduce the amount of distributions we pay. A default of a tenant on its lease payments to us would cause us to lose the revenue from the property and force us to find an alternative source of revenue to meet any mortgage payment and prevent a foreclosure if the property is subject to a mortgage. In the event of a default, we may experience delays in enforcing our rights as landlord and may incur substantial costs in protecting our investment and re-letting the property. If a lease is terminated, there is no assurance that we will be able to lease the property for the rent previously received or sell the property without incurring a loss. A default by a tenant, the failure of a guarantor to fulfill its obligations or other premature termination of a lease, or a tenant’s election not to extend a lease upon its expiration, could have an adverse effect on our financial condition and our ability to pay distributions.

- 13 -

We may change our investment objectives without seeking stockholder approval.

We may change our investment objectives without stockholder notice or consent. Although our Board has fiduciary duties to our stockholders and intends only to change our investment objectives when our Board determines that a change is in the best interests of our stockholders, a change in our investment objectives could reduce our payment of cash distributions to our stockholders or cause a decline in the value of our investments.

We may not be successful in identifying and consummating suitable investment opportunities.

Our investment strategy requires us to identify suitable investment opportunities compatible with our investment criteria. We may not be successful in identifying suitable opportunities that meet our criteria or in consummating investments, including those identified as part of our investment pipeline, on satisfactory terms or at all. Our ability to make investments on favorable terms may be constrained by several factors including, but not limited to, competition from other investors with significant capital, including non-traded REITs, publicly-traded REITs and institutional investment funds, which may significantly increase investment costs; and/or the inability to finance an investment on favorable terms or at all. The failure to identify or consummate investments on satisfactory terms, or at all, may impede our growth and negatively affect our cash available for distribution to our stockholders.

If we cannot obtain additional capital, our ability to make acquisitions and lease properties will be limited. We are subject to risks associated with debt and capital stock issuances, and such issuances may have adverse consequences to holders of shares of our common stock.

Our ability to make acquisitions and lease properties will depend, in large part, upon our ability to raise additional capital. If we were to raise additional capital through the issuance of equity securities, we could dilute the interests of holders of shares of our common stock. Our Board may authorize the issuance of classes or series of preferred stock which may have rights that could dilute, or otherwise adversely affect, the interest of holders of shares our common stock.

Further, we expect to incur additional indebtedness in the future, which may include a new corporate credit facility. Such indebtedness could also have other important consequences to our creditors and holders of our common and preferred stock, including subjecting us to covenants restricting our operating flexibility, increasing our vulnerability to general adverse economic and industry conditions, limiting our ability to obtain additional financing to fund future working capital, capital expenditures and other general corporate requirements, requiring the use of a portion of our cash flow from operations for the payment of principal and interest on our indebtedness, thereby reducing our ability to use our cash flow to fund working capital, acquisitions, capital expenditures and general corporate requirements, and limiting our flexibility in planning for, or reacting to, changes in our business and our industry.

We may never reach sufficient size to achieve diversity in our portfolio.

We are presently a comparatively small company with a modest number of properties, resulting in a portfolio that lacks geographic and tenant diversity. While we intend to endeavor to grow and diversify our portfolio through additional property acquisitions, we may never reach a significant size to achieve true portfolio diversity. In addition, because we intend to focus on single-tenant properties, we may never have a diverse group of tenants renting our properties, which will hinder our ability to achieve overall diversity in our portfolio.

The market for real estate investments is highly competitive.

Identifying attractive real estate investment opportunities, particularly in the value-added real estate arena, is difficult and involves a high degree of uncertainty. Furthermore, the historical performance of a particular property or market is not a guarantee or prediction of the property’s or market’s future performance. There can be no assurance that we will be able to locate suitable acquisition opportunities, achieve our investment goal and objectives, or fully deploy for investment the net proceeds of any offerings.

Because of the recent growth in demand for real estate investments, there may be increased competition among investors to invest in the same asset classes as our company. This competition may lead to an increase in the investment prices or otherwise less favorable investment terms. If this situation occurs with a particular investment, our return on that investment is likely to be less than the return it could have achieved if it had invested at a time of less investor competition for the investment.

We are required to make a number of judgments in applying accounting policies, and different estimates and assumptions in the application of these policies could result in changes to our reporting of financial condition and results of operations.

- 14 -

Various estimates are used in the preparation of our financial statements, including estimates related to asset and liability valuations (or potential impairments) and various receivables. Often these estimates require the use of market data values that may be difficult to assess, as well as estimates of future performance or receivables collectability that may be difficult to accurately predict. While we have identified those accounting policies that are considered critical and have procedures in place to facilitate the associated judgments, different assumptions in the application of these policies could result in material changes to our financial condition and results of operations.

We utilize, and intend to continue to utilize, leverage, which may limit our financial flexibility in the future.

As of December 31, 2020, we had a secured non-convertible promissory note to the Clearlake Preferred Member for $1.1 million that is due on December 16, 2021 and bears an interest rate of 10%. The loan is repayable without penalty at any time. The loan is secured by all of the personal and fixture property assets of the Operating Partnership.

As of December 31, 2020, we had one promissory note secured by our Cocoa Beach property for approximately $3.4 million requiring annual Debt Service Coverage Ratios (also known as “DSCR”) of 1.10:1.0, one promissory note secured by our Tampa Sherwin-Williams property for approximately $1.3 million requiring annual DSCR of 1.20:1.0, two promissory notes secured by our two Norfolk, Virginia properties totaling approximately $13.1 million requiring annual DSCR of 1.25:1.0 and one promissory note secured by our Washington, D.C., Alabama and Tampa, Florida properties for $11.3 million requiring quarterly DSCR of 1.25:1.0. The remaining promissory note totaling $1.1 million does not have a DSCR.

We make acquisitions and operate our business in part through the utilization of leverage pursuant to loan agreements with various financial institutions. These loan agreements contain standard affirmative and negative covenants, including prohibitions on additional liens on the collateral, financial reporting obligations and maintenance of insurance, in addition to the DSCR covenants described above. These covenants, as well as any future covenants we may enter into through further loan agreements, could inhibit our financial flexibility in the future and prevent distributions to stockholders.

We may incur losses as a result of ineffective risk management processes and strategies.

We seek to monitor and control our risk exposure through a risk and control framework encompassing a variety of separate but complementary financial, credit, operational, compliance and legal reporting systems, internal controls, management review processes and other mechanisms. While we employ a broad and diversified set of risk monitoring and risk mitigation techniques, those techniques and the judgments that accompany their application cannot anticipate every economic and financial outcome or the specifics and timing of such outcomes. Thus, we may, in the course of our activities, incur losses due to these risks.

You will not have the opportunity to evaluate our investments before we make them.

Because we have not identified all of the specific assets that we will acquire, we are not able to provide you with information that you may want to evaluate before deciding to invest in our shares. Our investment policies and strategies are very broad and permit us to invest in any type of commercial real estate, including developed and undeveloped properties, entities owning these assets or other real estate assets regardless of geographic location or property type. Our President and Chairman of the board has absolute discretion in implementing these policies and strategies, subject to the restrictions on investment objectives and policies set forth in our articles of incorporation. Because you cannot evaluate our investments in advance of purchasing shares of our common stock, our common stock may entail more risk than other types of investments. This additional risk may hinder your ability to achieve your own personal investment objectives related to portfolio diversification, risk-adjusted investment returns and other objectives.

We rely on information technology networks and systems in conducting our business, and any material failure, inadequacy, interruption or security failure of that technology could harm our business.

We rely on information technology networks and systems, including the Internet, to process, transmit and store electronic information and to manage or support a variety of our business processes, including financial transactions and maintenance of records, which may include confidential information of tenants, lease data and information regarding our stockholders. We rely on commercially available systems, software, tools and monitoring to provide security for processing, transmitting and storing confidential information. Security breaches, including physical or electronic break-ins, computer viruses, attacks by hackers and similar breaches or cyber-attacks, can create system disruptions, shutdowns or unauthorized disclosure of confidential information. In addition, any breach in the data security measures employed by any third-party vendors upon which we may rely, could also result in the improper disclosure of personally identifiable information. Any failure to maintain proper function, security and availability of information systems could interrupt our operations, damage our reputation, subject us to liability claims or regulatory penalties and could materially and adversely affect us.

- 15 -

We are an emerging growth company and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our common stock less attractive to investors.

For as long as we continue to be an emerging growth company, we intend to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies including, but not limited to, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. In addition, we have elected to use the extended transition period for complying with new or revised accounting standards. This election allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. As a result of this election, our financial statements may not be comparable to those of companies that comply with public company effective dates for such new or revised accounting standards. Further, we cannot predict if investors will find our common stock less attractive because we will rely on these exemptions. If some investors find our common stock less attractive as a result, there may be a less active trading market for our common stock and our stock price may be more volatile.

We will remain an emerging growth company until the earliest of (i) the end of the fiscal year in which the market value of our common stock that is held by non-affiliates exceeds $700 million, (ii) the end of the fiscal year in which we have total annual gross revenue of $1.07 billion or more during such fiscal year, (iii) the date on which we issue more than $1 billion in non-convertible debt in a three-year period or (iv) the last day of the fiscal year following the fifth anniversary of the date of the first sale of our common stock pursuant to an effective registration statement under the Securities Act.

We have experienced losses in the past, and we cannot assure you that, in the future, we will be profitable or that we will realize growth in the value of our assets.

From inception of our company through December 31, 2020, we had a cumulative net loss of approximately $4.2 million. Our losses can be attributed, in part, to the initial start-up costs and high corporate general and administrative expenses relative to the size of our portfolio. In addition, acquisition costs and depreciation and amortization expenses substantially reduced our income. As we continue to acquire properties, we anticipate high expenses to continue before we are able to achieve positive net income from our properties. We cannot assure you that, in the future, we will be profitable or that we will realize growth in the value of our assets.

We have paid and may continue to pay distributions from offering proceeds to the extent our cash flow from operations or earnings are not sufficient to fund declared distributions. Rates of distribution to you will not necessarily be indicative of our operating results. If we make distributions from sources other than our cash flows from operations or earnings, we will have fewer funds available for the acquisition of properties and your overall return may be reduced.

Our organizational documents permit us to make distributions from any source, including the net proceeds from equity offerings. There is no limit on the amount of offering proceeds we may use to pay distributions. To date, we have funded and expect to continue to fund distributions from the net proceeds of our offerings. We may also fund distributions with borrowings and the sale of assets to the extent distributions exceed our earnings or cash flows from operations. While we intend to pay distributions from cash flow from operations, our distributions paid to date were all funded by proceeds from our initial offering. To the extent we fund distributions from sources other than cash flow from operations, such distributions may constitute a return of capital and we will have fewer funds available for the acquisition of properties and your overall return may be reduced. Further, to the extent distributions exceed our earnings and profits, a stockholder’s basis in our stock will be reduced and, to the extent distributions exceed a stockholder’s basis, the stockholder will be required to recognize capital gain.

The limits on the percentage of shares of our common stock that any person may own may discourage a takeover or business combination that could otherwise benefit our stockholders.